I call it the Hollow Middle, but Knowledge@Wharton prefers “Disappearing Middle.” Here’s what, writing in their pages, the CEO of the Cambridge Group, identified as “a growth strategy consulting firm that is part of Nielsen,” has to say about it:

The Great Recession forced consumers to drastically rethink their purchase behaviors and, even though many have regained their financial footing in the five years since the downturn officially ended, those buying patterns have remained. As a result, more and more products are moving toward the “value” or “premium” ends of the spectrum, leaving a middle market that is struggling to remain relevant.

Not too many analyses have been written of the hollow or disappearing middle in Law Land (I suspect I may have authored many of them), so it’s edifying to look to other industries and see how the structural dynamics play out there. For myself, I find the following analysis essentially congruent with how Law Land is experiencing it (with appropriate nomenclature substitutes, of course). I invite any readers who may disagree to do so enthusiastically, either in a private email or through the comments. But let’s read on.

Our author starts by noting the increase in both “premium” and “value” products—reflecting what I’ve called elsewhere the “flight to quality” and simultaneously the “flight to economical” (all emphasis mine in what follows):

This month marks the five-year anniversary of the end of the Great Recession, but the 18-month economic downturn that began in December 2007 has had a more permanent impact on consumer purchase behavior than companies expected. That fundamental change in consumer behavior — coupled with a “hollowing out” of the market as more value and premium products become available — has resulted in the greatest challenge to the established market order in the last several decades. […]

The dramatic change in circumstances caused by the Great Recession has forced consumers to reconsider their choices in category after category. For many, the new choice stuck.

Consumers (read: clients) tasted the fruit of lower-priced products and in many cases were pleasantly surprised by the performance of the purchase. Lawyers tend to have a difficult time understanding that clients’ preferences could rationally be for “good enough,” in many situations, so let’s stick with consumer behavior for now, which exhibits precisely that type of rational selection.

This nicely explains why something that is, strictly speaking, “inferior” can still represent a compelling alternative:

While mainstream products may perform better than value products, the difference in performance created by a particular benefit (say, the freshness of beer, or convenience in banking) is not creating sufficient differentiated value to support the cost differential. Instead, it is adding material amounts of cost. What results is a preference, among many consumers, for the value offering – not necessarily because it is better and not only because it is less expensive, but because its price is more in line with its benefits than is the case with the mainstream product. This can be true even if the mainstream product improves its absolute performance advantage.

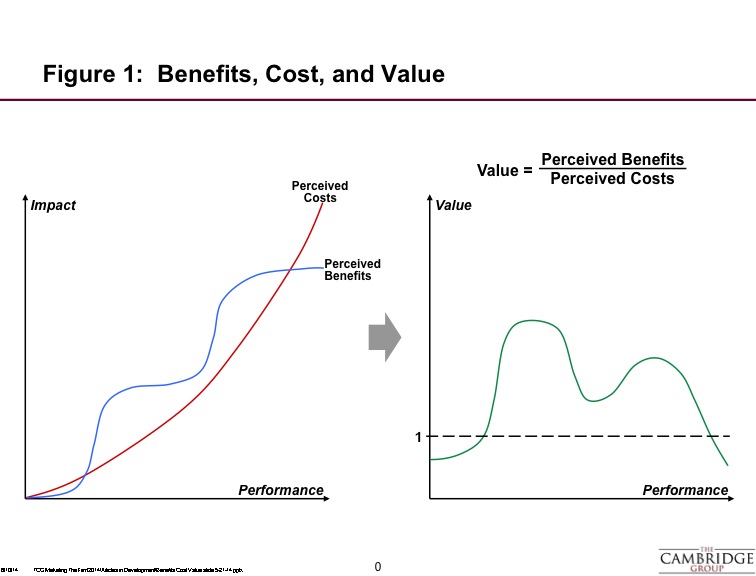

Here’s how the author visualizes it. The left-hand chart illustrates a fairly traditional cost/benefit tradeoff curve, where the two tend to march together more or less linearly: The more something costs, the greater its benefits in terms of impact. Quite familiar, and comforting to all of us aspiring to charge $1,000/hour.

The right hand chart, however, represents the new psychology—or more strictly speaking, and which matters far more profoundly, the new market behavior. On the right, it’s the ratio of benefits to costs that’s the pertinent metric (>1 is a win for the consumer, <1 a loss). And here, as you can see, both “too cheap” and “too dear” disappoint the client.

A favorite analogy for me, since you mentioned beer, is the effort by “Big Brew” to emulate the success of the craft brewing industry. Big Brew has seen flat to declining revenue for years while small, niche craft brewers are seeing double digit growth. Big Brew takes that half-step to moving up market by slapping a label on an undistinguished product seeking to tell the world, “we’re craft brewers, too.” It hasn’t worked too well.

Bruce:

Re Figure 1.

If I am reading this properly, it is important to understand that for these charts the entity rating cost and benefit (value on the right) is Client. The service provider has some vision (ideally, reasonably specific) about where its products/services lie. It is possible (likely?), for both Client and provider that value vs performance actually entails a range, not a point, both because performance may range (and/or vary in time) depending on specific resources available and also because different practice areas may have different cost-benefit characteristics. The first issue, on both sides, is how to make such an assessment in any meaningful way. The second issue for the provider is how to accurately understand how Client sees this chart and to determine how it may be possible to respond to improve the value case.

The qualitative graphs are fine for the conceptual-level, but the actual responses will depend on the ability (and effort) to quantify such matters and then to calibrate the curves to the Client’s vision of such matters. In doing the latter, the provider may well need to finding practicable ways to improve the value proposition.

If this seems roughly right (and it is what other industries do routinely, with greater or lesser success), perhaps in some later episodes AdamSmith,Esq. will pursue some of the approaches that may exist to would allow firms to appropriately measure the value they offer and how their internal estimations can be calibrated to the views of their clients?

Mark L.