We’ve written that leaving the office was trivial, at least in retrospect–“fire alarm’s going off, everyone leave the building”–but that returning is going to pose one of the most complex financial-cultural-operational-technological-recruiting & retention-organizational challenges that law firms have faced for years.

And not surprisingly, you hear a cacophony of views and predictions; more ink pixels have been spilled on this topic over the past few months than anything else by an order of magnitude.

We would like to try organizing the various issues into some sort of coherent framework and perhaps suggesting a few ways forward.

What we can say with a high degree of confidence

The emerging equilibrium once things settle down will not be:

- Everyone back in the office five days a week; not

- Everyone working remotely five days a week;

- Not a free-for-all what you want/when you want it;

- And when your lease comes up for renewal, you will downsize. Seriously downsize.

So if there’s going to be de facto some kind of hybrid model, how do we make the best of it? And how do we know what it’s going to look like? As the crack about predicting the future goes, you’re safe if you predict what will happen or when it will happen but not both.

(Speaking of when, a brief digression on the nasty and extremely unwelcome Delta variant: This is obviously causing companies, schools, universities, arts and sports organizations, and every other congregant venue to reconsider what plans they had in place as recently as two to six weeks ago. But–fully recognizing the human toll now being inflicted yet again when we are all so g.d. sick and tired of it–this will not change the long-run equilibrium. Delay, yes, different endpoint, no.)

Law firms entering uncomfortable (but welcome!) territory

Let’s back up for moment to how we got here: Starting around March 2020, we learned:

- Law firms can, believe it or not, pivot on a dime when it comes to functions as basic as how lawyers and staff do their (solo) “screen” work, meet with colleagues, connect with clients, “go to” court, collaborate on deals, form and disband project teams, recruit new hires, and much much more.

- But before we give the “firms” too much credit, the performers in this stunningly acrobatic adjustment were: Human beings. Humans are far more adaptable, far more quickly, than they’re commonly given credit for. This was not a top-down driven performance, it was bottom-up from the get-go.

- And if it could happen once, it could happen again–that’s the key learning here.

- We may have the opportunity to test that adaptability “in reverse,” as it were, when offices start reopening.

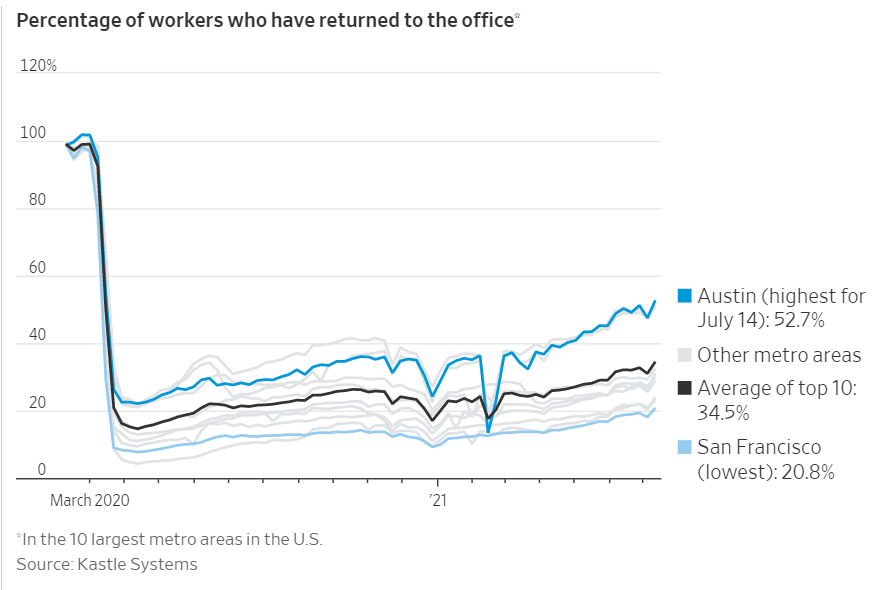

There will be no one-size-fits-all “solution.” Already, we have seen major metro areas diverge markedly in how quickly they are reoccupying their offices: Dallas, Houston, Austin, Phoenix and Miami, for example, at nearly 50% occupancy while New York and San Francisco are at 20% on a busy day. (These are commercial real estate industry figures, not Law Land specific figures, but let’s assume they’re a good approximation for us.)

Courtesy The Wall Street Journal

On that same note, a fascinating phenomenon was reported in The Wall Street Journal last week: “For Home Buyers, Length of Commute Drops in Importance.” The headline says it all, but data from major metros indicate house prices rising faster in remote areas than close in to the city centers. Zoom is here to stay.

So far, public announcements from firms are, well, all over the place

Some firms are saying they expect pretty much all hands back in the office this fall. Others (impressionistically, the tech-centric firms) have said everyone is free to keep working remotely for as long as, well, until we tell you otherwise. Some are telling their lawyers and staff to, essentially, figure it out for themselves: “Teams need to do what works best for them,” for example.

And perhaps the most common reality on the ground was captured by a client we were talking with this week who, when we asked what his firm’s return-to-the-office policy was, responded with one word, “Unclear.”

At Adam Smith, Esq., as regular readers know, we try to make a concerted habit of looking outside Law Land for learning from corporate America, multinationals, other professional service firms, and industries like tech, the media, insurance, manufacturing, and more. So what do we see there? The same phenomenon, frankly: Policies and realities are all over the place.

Generally speaking, tech is most comfortable with a very high quotient of remote work for as far as the eye can see. At the other extreme, all the B2C businesses that involve one-on-one personal service delivery have never been there and never will or could be. In short, firms are going to have to experiment, like it or not, with what works for them. Our industry’s favorite fallback/refrain when mulling a policy decision has long been “What are other firms doing?” If you’re looking for consensus, this will get you nowhere.

While we’re on the topic of variety-of-outcomes, here’s an other dimension we confidently predict will not be one-size-fits-all, and it applies within your own firm, not just to your firm vs. everyone else: The relative proportion of office:remote work will be driven strongly by:

- Generational differences: younger in the office more, to build their networks, learn the ropes (a/k/a “apprenticeship”), socialize and absorb and internalize the firm’s culture, etc.;

- Practice area differences: Tax lawyers may need to come in the office once or twice before your firm’s Holiday Party, but litigation associates will need a front-row, in-person seat to almost everything.

- Corporate/transactional may experience cyclic ups and downs:

- Office-heavy when teams are being put together, engagements scoped out, and marching orders determined.

- Remote-heavy during negotiations and drafting.

- And back to the office for final details, triple-checking everything, and closing.

Should clients have a say?

We all know what Morgan Stanley thinks: As reported by Bloomberg,

One of Wall Street’s top paid lawyers is telling his outside law firms to put an end to remote work and force their attorneys back to the office.

Eric Grossman, chief legal officer at Morgan Stanley, sent a memo Thursday to law firms and legal service providers encouraging them to improve client service by having lawyers and employees return to the office, according to a company official. Grossman’s memo suggested that those continuing to operate remotely risk their relationship with the financial services giant.

Grossman had potent air cover from none other than his CEO, James Gorman, who opined elsewhere that Morgan Stanley’ites “who want to make New York salaries…need to be in New York.”

In our considered opinion, how law firms staff their offices is none of their business. To float the unimaginable counterfactual, suppose one of New York’s white shoe elite issued a press release demanding that Morgan Stanley and Goldman Sachs bankers be in their midtown skyscraper five days a week if they want to keep their competitive edge and be entitled to the services of Said August Law Firm.

Or, less head-explody, suppose another high-profile GC announced that, now that we all know that hundreds of thousands of square feet of Class AAA office space is not, strictly speaking, a prerequisite to BigLaw getting its work done, their company would break off relations with any firm that didn’t cut waste by moving to a hoteling model in a Class B neighborhood.

Our first counterfactual might be hallucinatory, but the second is at least as plausible as Mr. Grossman’s imperious diktat and more economically rational. So, should clients have a say?

No.

But before leaving this beaten-to-death topic, have you noticed the same phenomenon we have? Namely, that all but one B2B industry is coming up with different approaches to the back-to-the-office drumbeat. Tech may be “liberal” in extending remote work plans, but at the same time Amazon, Facebook, and Google are committing to millions of square feet of long-term leases in New York, the creative industries are taking a, well, creative approach; and so on. No industry is speaking with one voice on what the world should be doing on this score.

Except one: Big banks and finance powerhouses. Not only are they speaking with one voice on “back in the office or else,” they are chiding the rest of the world to do the same. When you see an outlier like that, you (well, we) wonder what’s going on.

Permit me to share a hypothesis I first saw a few days ago in the newsletter of a lifelong New York commercial real estate industry insider. They began with the perfectly plain observation that:

Anyone who has seen the sparsely populated downtowns of major cities such as San Francisco, Boston, Chicago and New York knows that the commercial office property market is in jeopardy, even if apartment dwellers are coming back to enjoy the pleasures of city life.

So far so unexceptional.

But then there’s this:

Since office lease terms can be as long as 10 to 15 years, the risk to property owners is that as leases come due, tenants may be reluctant to renew them by taking the same amount of space for extended durations. …

Obviously, a significant drop in office leasing threatens the entire ecosystem: lending, securitization, equity ownership and real estate investment trusts, all of which are pillars of the real estate industry. This is a market well in excess of a trillion dollars and a backbone of our economy. Small wonder that one of the bulwarks of the system is trying to nip this budding problem in the bud, so to speak.

A major asset class for banks and large financial institutions is commercial real estate. LTV requirements (loan to value) of 75-80% are common for Class A space in major markets. And widespread reports from knowledgeable institutions have estimated the value of some major metro office buildings has taken a haircut of 20-25% or more. Do the math.

“This does not reflect the opinion of management” as they say (management actually has no opinion on this), but there you have it. My real estate friend’s thesis at least helps explain why Big Banks are an outlier all by themselves on this one.

Great, but what are we supposed to do?

I will close with a few concrete suggestions, which I hope you find constructive.

First, experiment with “core hours.” This practice has been in place for decades but invisibly, and now it has emerged center stage. Dropbox, Slack, and other companies have set times–say, between 10 am and 2 pm or 1 pm and 4 pm, when everyone has to be online and available for Zoom, project meetings, and other forms of collaboration. All other times are meeting-free zones.

Yes, of course, take time zones into account; you might even have different “core hours” different days of the week and different durations of those core times. Season to taste. They key is that the firm and lawyers and staff all achieve predictability within an autonomous and flexible framework.

Second, if you land on a fixed ‘expectation” of more than zero but fewer than five days/week in the office, do not make a required day Friday. Just don’t .

Third, face the reality that Covid is here to stay. As the Rector of Trinity Church/Wall Street wrote more poetically a year ago: “Beloved, we are in this for the long run.”

Covid is migrating from pandemic to endemic. That means only long-term, sustainable, minimally intrusive policies and practices are feasible–and that we have to get past our on-again, off-again spasms of panic and complacency with their changeable and sometimes arbitrary strictures. (Masks? Everywhere all the time? Some places for some people? Nowhere and for no one?)

There is one and only one way to get there. So:

Most important by far, require fully-vaccinated status for anyone (lawyers, staff, clients) who wishes to visit your office. Clifford Chance and (yes) Morgan Stanley have both announced such policies. Hospital systems, universities, major public venues, and–shock–the country of France are moving in this direction.

Why is this important? Because vaccines work. If we care about saving lives and avoiding human suffering, there is no substitute. The fact that they’re free, universally available (in the First World), and infinitely safer than getting Covid are extra benefits. Masks, social distancing, Lady Macbeth-handwashing: All are useful but palliative, and they were stopgap measures when we had no better tools. Now we do.

Testing, you ask? Experience has taught us that testing is tiresome, costly, error-prone, a damned nuisance, and doesn’t answer the key question: Is this person going to get seriously ill, end up in the hospital, or end up dead? And if someone does test positive–someone will–now what? “Everybody out of the pool!!”? That way lies insanity, if not insolvency.

A word on “breakthrough” Covid–cases in fully vaccinated people. Our first generation of mRNA vaccines is magically, almost unbelievably, effective: But they are not, as Dr. Anthony Fauci reminded us last week, “invincible.” Yes, Covid can again attack, no matter what–at this stage. The question is not whether they’ve achieved perfection in a world of 3-billion+ vaccinated human beings, but what protection they offer: That’s where they show their strength.

Human beings get sick; what matters is how sick they get and if they’re like to die.

The data showing how effective vaccines are on this score is ubiquitous, and a “graphic” example is a map of the US showing hospitalizations and deaths correlated with those who hadn’t been vaccinated. “We have a pandemic of the unvaccinated,” to coin a phrase.

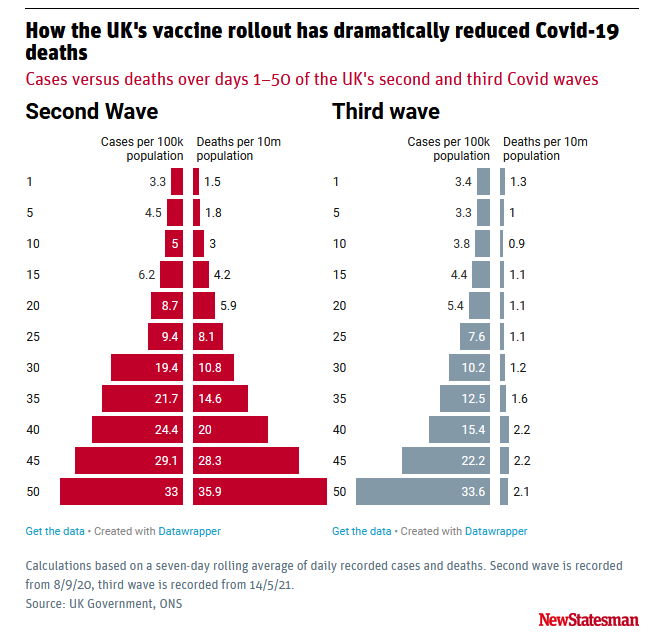

Here’s my favorite chart on this, from the fertile editors at Marginal Revolution:

This shows cases vs deaths over the first 50 days of the UK’s second wave (starting in August 2020–no vaccines yet available) vs. its third wave (starting in May 2021–vaccines available for months beforehand):

Source: UK Government, Office of National Statistics: Seven-day rolling average of recorded cases and deaths.

As a mentor once said, “Numbers don’t have opinions.”

To the extent your firm can move the needle on vaccinations, even slightly and in your own backyard, why would you not do this? You have only your lawyers, staff, and clients to lose. And then get back to work.

Courtesy Unsplash