Universally, everyone is hearing that firms plan to make significant cuts in real estate spend starting, well, starting as soon as the next office lease comes up for renewal.

How “substantial” might those cuts be?

You would think a massive and sophisticated industry like BigLaw would have copious data breaking down overhead expenses, but if you thought that you would be a tyro in our world. Of course there’s no centralized or even consistent data source! The best one can do is restate the conventional wisdom to the effect that “occupancy” costs (office rent/leases, maintenance, security, furnishings and fixtures, utilities, etc.) is the second largest single category of spending for law firms, after salaries and benefits for lawyers and staff.

On the other hand, some suggestive data and some relatively hard figures are available from, where else, sources outside Law Land. According to Law Firms are Dumping a Significant Amount of Office Space (published in October 2020), in 2019—need I remind anyone, the last full year before the pandemic—law firms accounted for 5.9% of all office leases signed in the US.

Judging by the context, presumably the unit of measure for that 5.9% figure is square feet, but it could be lease value by $$, and unfortunately the authors don’t exactly make it clear for us which it is. I offer this distinction because unlike some distinctions it is one with a difference; one can venture with a high degree of confidence that some industries’ share of square footage exceeds their share of lease expense (warehouses, anyone?) and for other industries the reverse holds (and yes I’m guessing law firms are in Column 2).

In markets like Adam Smith, Esq.’s home (Manhattan), CBRE ranks law firms the fifth largest industry in terms of signing up for space, at 819,735 sq. ft. during 2019.

But there’s more.

A relative treasure trove of data and perspective comes from an annual “Legal Sector Benchmark Survey,” (new to me but now in its seventh year), compiled by the real estate services firm Cushman & Wakefield under the direction of Sherry Cushman, Executive Managing Director of the firm and vice chair of the legal sector advisory group.

Better yet, we have some historic data: Around the time of the GFC (say, a decade+ ago), firms allocated 1,200—1,400 square feet per attorney. As of 2019, new law firm leases were coming in at a little over half that, closer to 700 square feet per attorney. The guesstimate offered in the article for the post-Covid-10 “target ratio” is said to be more like 400 sq. ft. per attorney—or even less.

If you take these figures at face value, we’ve cut our per-lawyer space by 50% over the past 10-12 years and we’re about to cut it by another 40% or more. According to Ms. Cushman, new law firm leases signed in 2018 and 2019 (moves to entirely new space, that is) averaged 29% smaller than the old space, and even renewals (in the same space) took a typical haircut of 19% of the original space.

It’s reasonable to imagine that as the world begins to emerge into the sunny Alpine meadows of the post-Covid world (admit it—Covid fatigue is a real thing), firms will feel more confident about re-evaluating their long-term space needs. We’ll have a grip on who and how much “WFH” there will be, and since office leases are among the longest time horizon financial decisions that law firms regularly make, careful analysis will, we can only hope, be brought to bear.

To that point, Cushman & Wakefield makes a strong and critical point: They forecast that 2021 and 2022 will see “a large number of early lease restructures and space givebacks on a widespread basis [across] the U.S.” And get this (emphasis supplied):

This “right sizing” of the legal sector, that currently occupies two to three times the square footage per employee than other industries, is a sector correction that is long overdue. Our surveys have consistently shown that firms have begun to downsize and be more efficient in their use of space, but entrenched practices allowed firms to be complacent and resistant to this change. Technology advancement, a shift to the younger generations gaining prominence in the workforce, and COVID-19 changed those attitudes. In 2025, it is anticipated that 56% of the U.S. prime working aged employees will be millennials. This statistic has and will continue to have significant impact on the legal sector and its real estate decision-making for the future.

We’re not done.

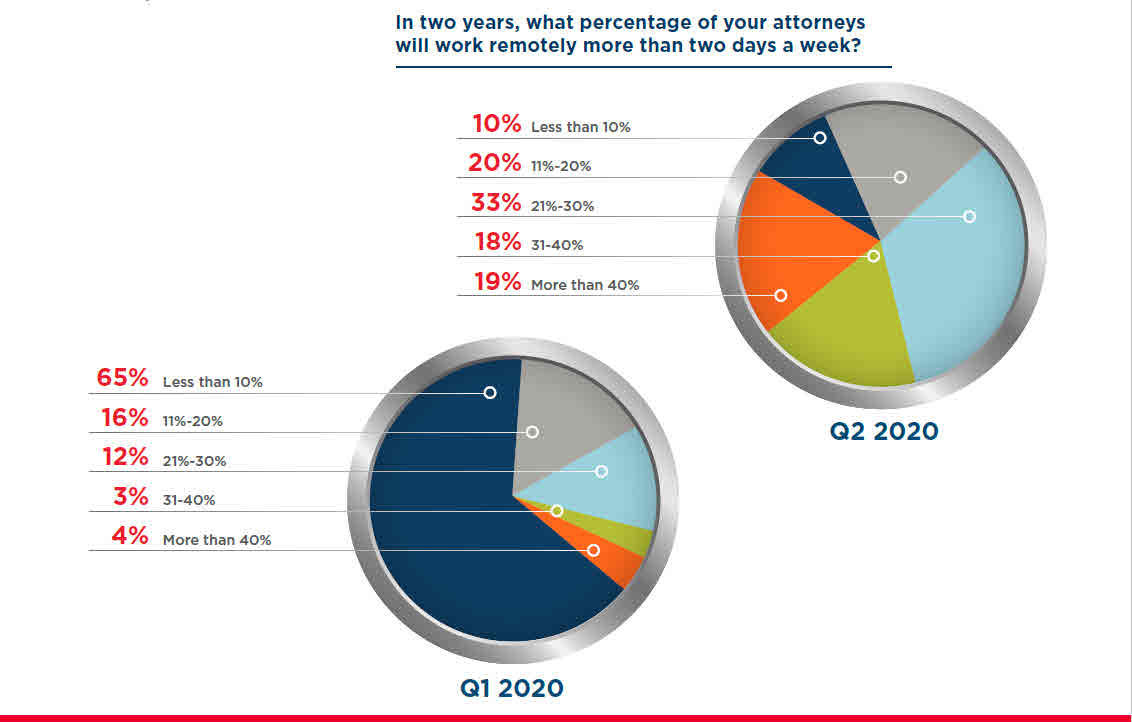

Here’s one of the most dramatic visualizations I’ve seen of how quickly BigLaw attitudes changed towards remote working. Note that this is the same question asked of (basically) the same people in January through March of last year and again in April through June:

Courtesy Cushman & Wakefield

It speaks for itself, but some of the drastic changes demand highlighting: In terms of the percentage of lawyers working remotely “more than two days a week” (which sounds like more than half the time to me):

- >40% quintupled

- <10% shrank by 85%

- And more than one-third quintupled from 7% to nearly 40%

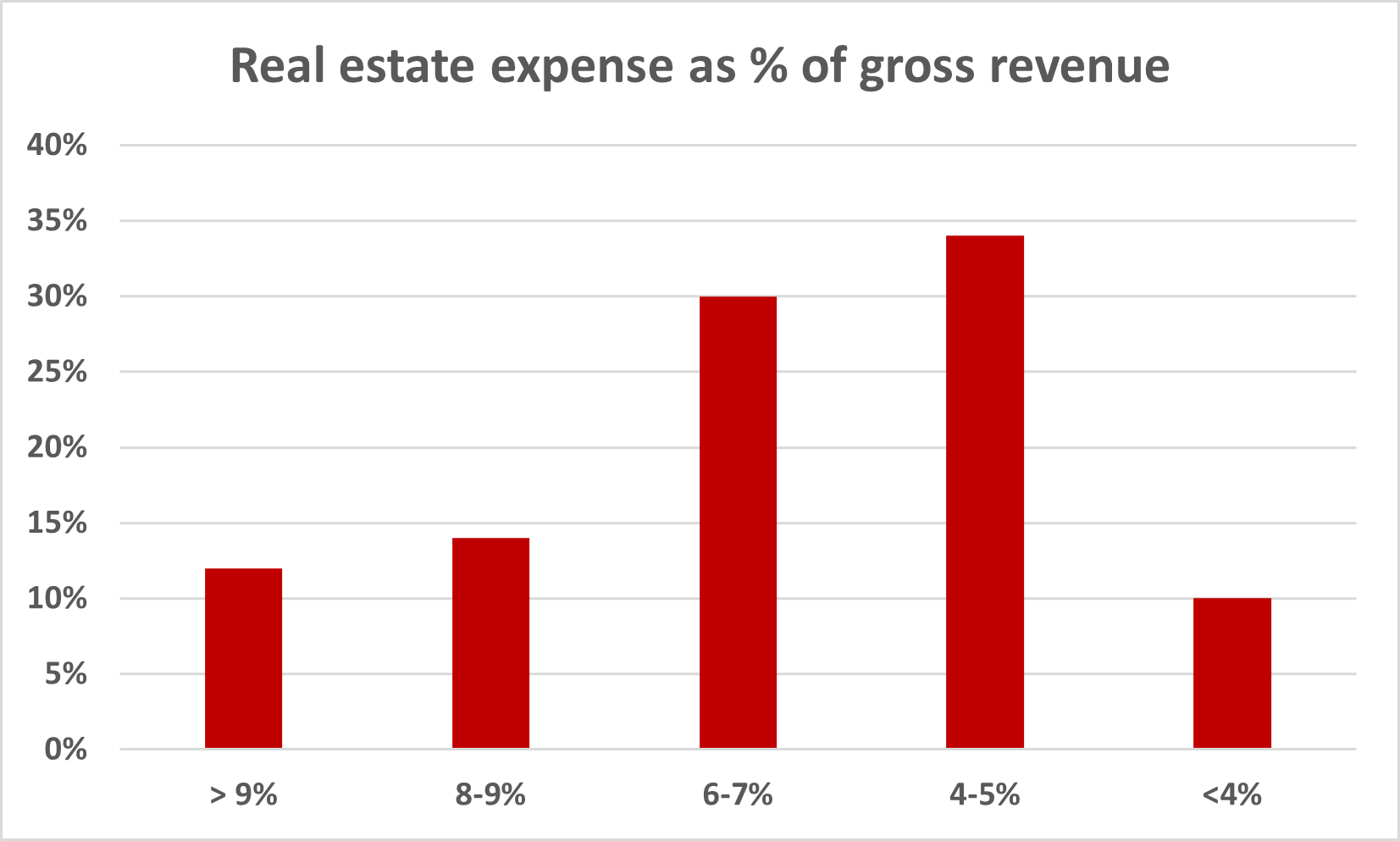

Earlier I mentioned that lore in our data-drought-stricken industry is to the effect that real estate is the second largest category of expense. Well, Law Land may exist on a barren Martian-surface data landscape, but the commercial real estate industry does not. Here’s what the Cushman & Wakefield survey reports about law firms’ spend on real estate as a percentage of their annual gross revenue:

Adam Smith, Esq. adaptation of Cushman & Wakefield data

This does not give us an industry average—and it would be surprising to the point of incredible if firms clustered much more tightly on this metric—but it gives us a compass point to estimate with. Eyeballing this distribution I’m going to make the assumption for purposes of the rest of this column that the “average” industry-wide is 6% of annual gross revenue going to real estate. The gross revenue of the 2020 AmLaw 200 was $124.6-billion, so that means real estate cost those firms about $7.5-billion. That’s A Big Number, but to get an instinctive notion of how big exactly, consider that domestic US Hollywood box office revenue has averaged about $10—11 billion annually over the last couple of decades. Our real estate spend isn’t far behind that (and that’s just the AmLaw 200, not the industry).

How much of this might we save in a post-Covid world?

It’s very early to see much real data on this, but one point is hammered home in the Cushman & Wakefield report repeatedly, and we here are hearing similar stories: If you’re going to need less space, it might as well be nice.

In other words, you might move from Class B+ or A- space to AAA and hold your spend level constant or even see it go down. The moon shot Hudson Yards development on the far West Side of Manhattan is mentioned by name more than once as an example of “super amenitized” space (I did not make that coinage up, folks, but I’d apologize to you if I had), and firms like Latham, Milbank, and Skadden have already planted their flags there.

[It may seem odd or even perverse to read that goods and services that cost more can be desirable by virtue of that, but the phenomenon is fairly widespread in real life and even has a name: “Veblen goods,” namely items that are more desirable because and not in spite of their cost.]The second point is simply the first real piece of data we’ve seen. UK firms, as most Adam Smith, Esq. readers know, are required to file annual financial statements with Companies House and Allen & Overy just did so. Key data point for purposes of today? The firm’s total (capitalized) lease liability at the end of April 2020 was stated as £559.3m but A&O give it a haircut of £155.3 in their current filing—or about 28%. The New York Times recently noted in an extensive front-page story (“Remote Work is Here to Stay; Manhattan May Never be the Same”) that Lowenstein Sandler may not renew the lease for its 140-lawyer office at Sixth Avenue and 50th Street.

So this brings us to your homework assignment.

If you’re not going to spend as much $$ on real estate, what are you going to do with the savings? Remember that $$ out the door to supporting real estate is never seen again and is pure “consumption” (spent this period for services delivered this period, with no market or tail or terminal value). You could, and I suppose some of you will, simply distribute a large share of it to partners at year-end.

But I have a different idea: What if you could repurpose a lot of that money to investment instead? What investments would you make? Would you even create a “retained earnings” entry on your balance sheet and begin saving for that rainy day or that opportune stroke of lightning that must be seized or lost forever?

In the context of what we’ve learned during Coronatide and what we know will be true going forward, I think there’s one compelling priority, whether it’s all of the saving or a portion. Whatever you foresee, if you think spending the same or less on this is smat management going forward, we should talk.

And the category of spending I have in mind? Technology.

We live and die by knowledge, intellectual and social capital, responsiveness and speed, ability to scale up resources at a moment’s notice, and densely connected human networks. Here’s a pithy, realistic prediction from Daniel Pinto, JPMorgan’s co-president and chief operating officer (interviewed on CNBC last month):

“Going back to the office with 100 percent of the people 100 percent of the time, I think there is zero chance of that. As for everyone working from home all the time, there is also zero chance of that.’’

Bottom line: You do not need nearly as much real estate as you thought a year ago. You need far more technology than you thought a year ago.

Let the games begin.

For information: US rate of R&D investment:

https://www.aaas.org/news/new-data-says-us-rd-has-topped-3-gdp-first-time-ever?et_rid=35078877&et_cid=3718380

Short version: > 3% of GDP. Obviously, comparability of Law to other ventures that have R&D needs thought (ASE has been raising this for years), but in keeping with the current post, thinking about how to use available funds toward a stronger future is as worthwhile for professional services as for anyone else.

Nice dataset, Mark: Thanks! Prompts a few thoughts:

Thanks as always!