I come not to bury the office, but to praise it.

Kind of.

The Covid-19 pandemic has changed human and economic behavior in a myriad of ways, and we can all stipulate that overall we’ve been living through a period that has inflicted tragedy at the human level, wreaked devastation and smashed dreams across broad swaths of the global economy, and exposed naked political cravenness and rank ineptitude in every region of the world. Tone-deaf to even entertain the possibility of a silver lining, no?

And yet: We have learned many lessons that, I for one hope, we will remember and take with us on the other side of this. First and foremost I would nominate our collectively experiencing a vivid reminder of how fabulously adaptable human beings are. For today’s purposes, it’s not about setting up restaurant patios in a traffic lane on Broadway or plexiglass between you and the Starbucks barista, it’s about how the [white collar professional] world of work pivoted in 24-72 hours from everyone in the office all the time to WFH, Zoom, and now permanent/customized at-home office spaces.

A quite different one that we’ve written about previously centers on the second greatest expense category (after people) for almost any law firm: Office space and occupancy costs. It can add up to a lot of money, since we accept nothing short of Class A space in expensive and hyper-expensive metropolitan areas across the world. If it hasn’t gotten your attention, it will.

A few basic data points by way of orientation. I will focus on our home town because, among other things, lots of data is available, I haven’t just read about it but lived and experienced it, it’s as massive a natural experiment on this topic as one is likely to find, and we know some local resources when you do get around to thinking hard about your office.

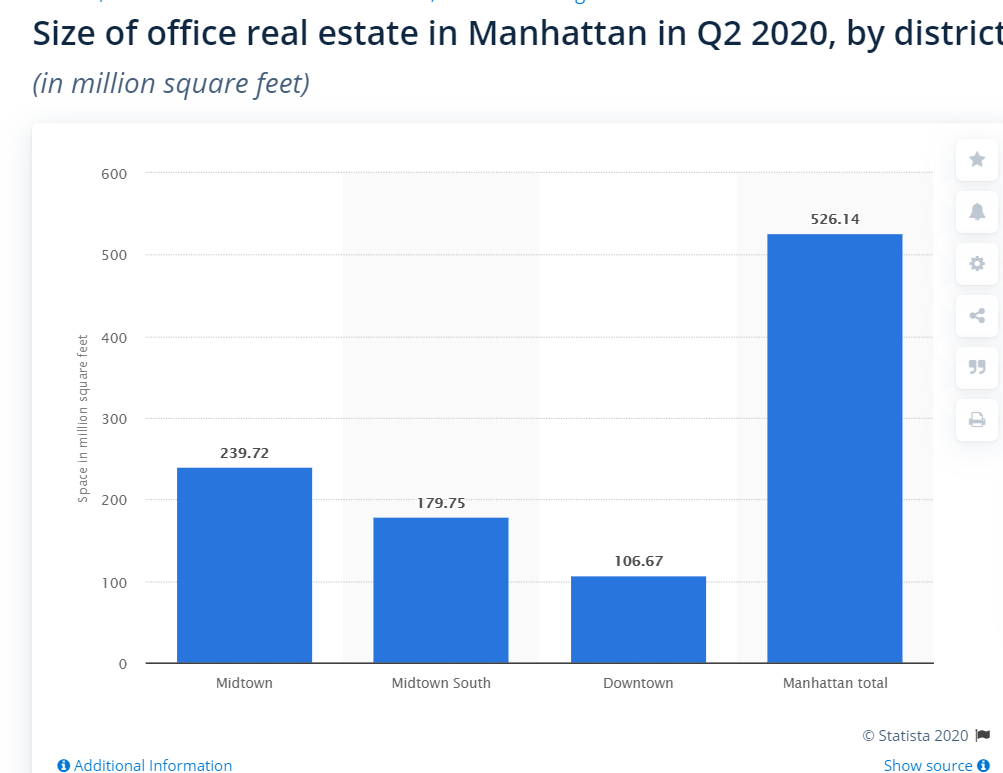

The size of the market:

Courtesy Statista

Asking rent for Class A office space in 2Q 2020 in midtown Manhattan averaged $89.18/square foot. The overall Manhattan-wide average was $85.12, and Midtown South was the priciest area at $98.28.

Getting a little more parochial, a late 2019 report on “Legal Sector Trends in Manhattan” published by CBRE said that the 1,801 law firms in its dataset took up 34.87 million sq. ft. of office space accounting for 9.3% of the total RSF in Manhattan.

If we assume for simplicity that all the law firms are in Midtown, the extrapolated amount they spend annually on rent is $3.11-billion. “Real money.” (In our experience, “Midtown South” a/k/a Flatiron-Chelsea is too chic for most law firms, plus it tends not to be where their key clients are).

So those are the facts.

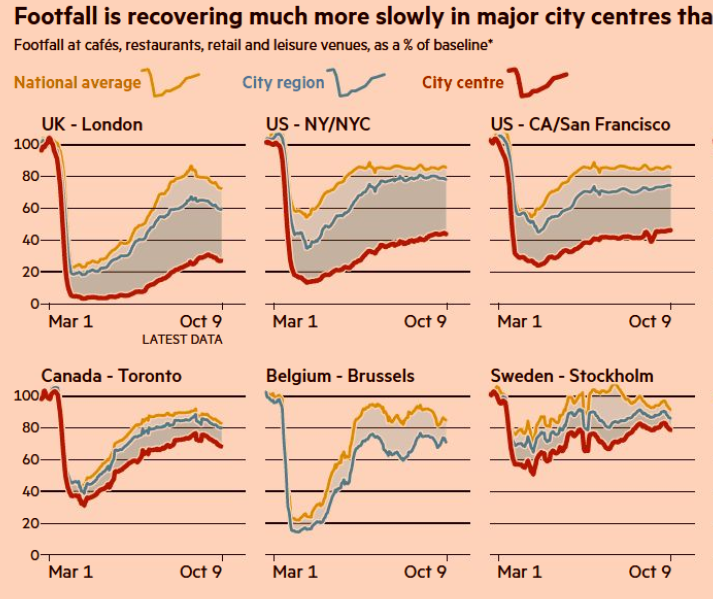

Now let’s look at what Covid-19 has done to foot traffic in a few major metros:

Courtesy The Financial Times October 2020

The question this poses for a venue such as Adam Smith, Esq., is what are the economic consequences of the combination of this massive, not-permanent-but-not-entirely-temporary, change in human behavior combined with the miraculous and unimaginable discovery (“realization?”) that not everyone needs to be in the office all the time.

Now, regular readers know that we’ve already essayed our thoughts on what The Office on The Other Side will look like and what functions it will be optimized to perform. (See the first link in this article.) We don’t believe that 100% of your office occupants as of February 2020 will return every day all the time, and we don’t believe you can give all your office keys to your landlords and declare yourself an all-WFH-all-the-time firm. You will still need and very much want offices, but very different from the ones you had.

In short: Your new office will not be designed as a space where dozens and dozens of people can go into smallish rooms, shut the door, and open a laptop. It will be designed as a [smaller overall] space optimized to host and encourage the activities that human beings have learned over the past 200,000 years or so are best or can only be performed in person: Close collaboration, socialization, apprenticeship and mentoring, intensive knowledge transfer and learning, building interpersonal trust, meeting/greeting/sizing up others as only the massive bandwidth of in-person interactions can provide, and so on. Think highly successful Silicon Valley firm, not Taylorism.

Back to the economics.

What we have experienced is a one-time, powerful and substantial, “step change” reset of the price of high end commercial real estate in major metropolitan centers like New York. That’s already in the past; whether or not the market is recognizing it yet or not in actual transactions (there are almost none), it’s in the history books and probably was by about mid-March on this Island where I live and work.

You rarely see, much less live through, such dramatic step-change resets of asset prices, and particularly not with such a massive asset class as Class A office space in New York City.

So how might this play out?

Well, so far it hasn’t played out. Every story you see about when corporate America—or Law Land—plans to be “back in the office” pushes that date farther out. Like I said, we haven’t seen any transactions yet. But smart tenants (that would be readers of Adam Smith, Esq.) are already making plans to downsize/re-size/optimize/smarten up their offices over time.

Landlords, by contrast, so far as all media reports and personal conversations we’ve had reveal, are in firm denial. (Come to think of it, they may be about to embark on the seven stages of grief.)

For example: “’I’ve been really pushing the CEOs to bring people back into the office,’ Jeff Blau, the developer behind the Hudson Yards project, said. ‘I’ve been using a little bit of guilt trip and a little bit of coaxing.’” (August 2020: Fairly representative in your editor’s humble opinion.)

Ruth Colp-Haber, President of Wharton Property Advisors, an NYC-based commercial real estate advisory firm, sums it up much more bluntly (I somewhat paraphrase Ruth, who we know):

It’s not enough to just spiff up the trophy buildings with new ventilation systems and clever signage, sanitizers and no touch gadgets. Landlords need to recognize that over a century of landlord hegemony is over; they need to start thinking like entrepreneurs building a business rather than sitting complacently waiting for tenants to walk in. They need to be partners with their tenants rather than mere rent-seekers.

When a massive asset class experiences an enduring step-change in value, the economics of the fallout are easy to describe: Essentially, the demand curve shifts dramatically downward. At any given price, a smaller quantity of the asset will clear the market. The new equilibrium will without question be at a lower overall price—although it’s unknowable as a matter of theory whether the total quantity of the asset clearing the market will be a lesser or a greater quantity. (That depends on what creative alternative uses the owners and renters/buyers of the asset figure out they can put it to.)

Driving this tectonic shift is the supremely consequential discovery/realization that occurred within the white-collar professional world around the second week of March here and thereabouts in the rest of the world. A lot of us can work from home a lot of the time. One veteran of the NYC market puts it this way:

“The tether between work and home just got a lot longer,” said Jonathan Miller, a New York real estate appraiser. That shift is already increasing buyer demand in more affordable markets beyond the city center. [Disclosure: We know Jonathan.]

Even that is still evolving, of course: People are beginning to wonder, “Well, if WFH from the Upper West Side or Montclair, NJ is so seamless, how about the Berkshires, Cape Cod, Vermont, Jackson Hole, Sedona, ….”

The economic label for the implications of this discovery about the “optionality” of everyone being in the office all the time is that the world realized there are substitutes for the office article of faith and concomitant demand. A key characteristic of an effective and useful substitute Beta for prior activity Alpha is that no one ever forgets Beta is an option. Alpha loses market share, permanently.

You, dear Class A office tenant, have an opportunity. Step-change asset price shifts are by definition asymmetric, and you are on the winning side of this trade.

Landlords may be in denial, and the publicly available evidence supports they remain staunchly there.

But collectively they own massive amounts of square footage worth materially less than it was worth in January. As the old joke goes, “If you owe your bank $10,000 and can’t pay, you have a problem. If you owe your bank $100-million and can’t pay, your bank has a problem.”

Guess who has a problem here?

Courtesy CBRE