Say what you will about the “social distancing” clampdown put in place all over the world, but you will never find stronger consensus among economists about anything than this: They are desperately needed if we are to get back on our feet again.

Some of you may know of the University of Chicago Booth’s “Initiative on Global Markets,” which is a fascinating window into the consensus thinking (or lack thereof) of leading economists on key issues du jour. Here’s how they describe it (I quote in full to do it justice):

This panel explores the extent to which economists agree or disagree on major public policy issues. To assess such beliefs we assembled this panel of expert economists. Statistics teaches that a sample of (say) 40 opinions will be adequate to reflect a broader population if the sample is representative of that population.

To that end, our panel was chosen to include distinguished experts with a keen interest in public policy from the major areas of economics, to be geographically diverse, and to include Democrats, Republicans and Independents as well as older and younger scholars. The panel members are all senior faculty at the most elite research universities in the United States. The panel includes Nobel Laureates, John Bates Clark Medalists, fellows of the Econometric society, past Presidents of both the American Economics Association and American Finance Association, past Democratic and Republican members of the President’s Council of Economics, and past and current editors of the leading journals in the profession. This selection process has the advantage of not only providing a set of panelists whose names will be familiar to other economists and the media, but also delivers a group with impeccable qualifications to speak on public policy matters.

Finally, it is important to explain one aspect of our voting process. In some instances a panelist may neither agree nor disagree with a statement, and there can be two very different reasons for this. One case occurs when an economist is an expert on a topic and yet sees the evidence on the exact claim at hand as ambiguous. In such cases our panelists vote “uncertain”. A second case relates to statements on topics so far removed from the economist’s expertise that he or she feels unqualified to vote. In this case, our panelists vote “no opinion”.

It should come as no surprise to regular readers that I’m a longtime fan of the “IGM Forum,” and I’ve never seen people line up so thoroughly on one side.

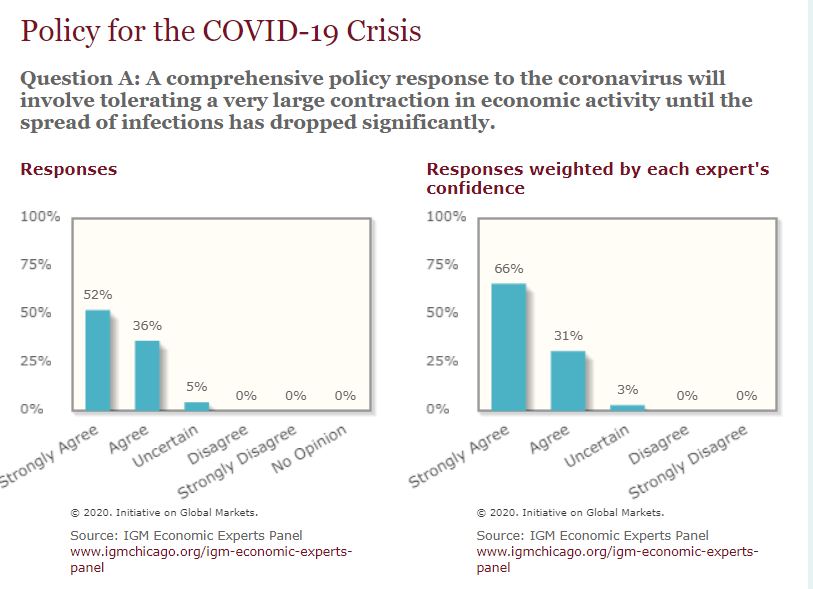

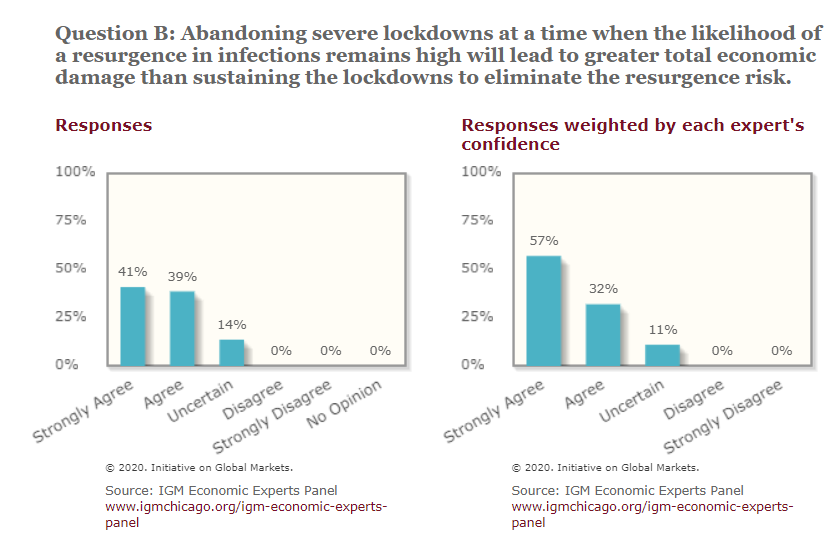

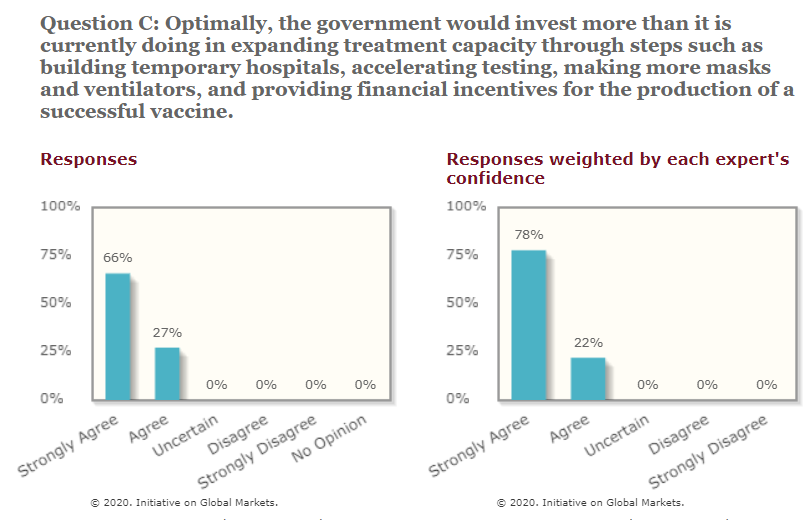

Here’s the data:

So in a nutshell we have powerful agreement that (a) we need to tolerate an enormous hit to economic activity (b) for longer than some might like (c) and at the same time write unlimited checks to expanding treatment capacity (short of fraud, as always).

Count it as a small blessing: Reassurance from non-epidemiological quarters that social distancing, strictly enforced for a long time, is going to be worth it eventually.

Midrange Guy:

You are of course completely correct that in the Golden Era of single-tier partnerships (and zero lateral movement, which I think is both conceptually and structurally connected) partners were paid in profits and associates and staff in W-2’s. (Footnote: Partners might get an advance draw during the year against their year-end profit distribution but it was not “additional” comp, it was just to let them pay their monthly fixed expenses; it would be deducted from their profit share at year-end as an advance against same.)

Now that equity/non-equity/”income”/of counsel/&c. has blurred all these lines, I found in composing the article that it was convenient–and perhaps admittedly a bit lazy–to blur those lines in my composition as well.

The truly interesting behavior to keep one’s eye on now, I predict, will be whether equity partners start complaining that they never bargained for the downside of being an owner in crummy economic times. Wouldn’t that be rich?