More so of late, but for some time, we’ve been harboring the suspicion that the glory days of the high-leverage model are over. Could we be seeing the end of leverage?

Of course, many management fads fashions tend to come and go, which is why we at Adam Smith, Esq. have always declared our primary membership affiliation to be among the empiricists and the agnostics. “Let us actually take a hard look at what’s going on, and then and only then will we offer a diagnosis and prescription.” Something like that. And in this vein, while we’ve been harboring the “end of leverage” hypothesis for some time, we are beginning to see the first whiffs of data appear in its support. Data later, but first back to the dominance of the leverage model for so long.

[An irresistible digression: For at least a couple of decades during the post ~1980 boom era, a legal consulting firm became known, understandably if somewhat simplistically, for recommending “Merge!” to any and all clients: A universal solvent for all problems. Life would be easier that way, wouldn’t it?]Leverage as an almost per se desideratum has had a long and heretofore mostly healthy run. After all, it’s based on elementary arithmetic: The more high-margin associates I can have churning away below-decks for me, the more profits they’ll spin up into the clean cool air of the partnership. If one is good, two are better, and if two are good, etc.

But note the unspoken assumptions behind this, which have always been lurking in the background whether or not we cared to articulate them:

- First and perhaps most obviously, it assumes clients will willingly pay substantial amounts, today and into the indefinite future, for these (by hypothesis) less experienced, early-in-their-career, lawyers.

- Hand in glove with “paying” is the embedded assumption of a handsome level of realization; that clients won’t push back relentlessly on rates or hours or both.

- Somewhat more subtly but no less critically, it assumes a ready supply of willing, capable-enough, and frankly somewhat fungible human beings to toil as associates for as many years as the firm and the associates can stand it, with everyone on all sides aware but sworn to silence on the awkward topic of how many will actually be rewarded with partnership.

- And finally, it assumes something that we never thought until fairly recently could be challenged: That clients would have no choice about, or would prefer to, “bundle” all the legal work comprising a matter within the walls of the law firm itself rather than disaggregating it or picking and choosing the best supplier for each component of the engagement.

Now, need we point out that all four of these assumptions are coming into question or worse: 1. and 2. are almost risibly passe. Prohibitions on first-years appearing on invoices are a commonplace. You may unconsciously assume that a 20% drop in rates+hours+realization on associate X takes 20% off their profitability to the partnership, but not so fast. The 20% haircut comes entirely out of profits. The associate’s salary, benefits, overhead allocation, and everything else didn’t, upon inspection, accommodatingly drop 20% as well; they are unchanged. So 1. and 2. have teeth.

As for 3., the number of qualified, especially highly qualified, college graduates applying to law schools has been on close to a decade-long decline. It may be bouncing around a bit lately–labor markets tend to be noisy and subject to short-term fluctuations–but when it’s reliably reported that some of the Most Upper of the Upper Crust law schools in the nation are struggling to find enough qualified applicants to fill their entering classes, the world has changed. (Straw in the wind: Harvard Law dropping the LSAT requirement? And what might that imply, do you suppose? Just sayin’.)

Finally, 4. Aaah, yes, 4. Welcome to the era of NewLaw, “Alt Law,” “legal corporations,” “ALSP’s (alternative legal service providers),” or whatever nomenclature we ultimately come to rest with. As with the double whammy of rates/hours and realization shrinking not your expenses across the board but coming straight out of profits, so every $1.00 clients spend with a NewLaw provider takes more than $1.00 off the law firm’s top-line. (How do we know? Because clientd do it to save money. QED.)

As for the size of the “multiplier,” you can make that into a parlor game of your own, but my best guess is about $3.00, based on a variety of sources and indicators. Call it $2.00 to be conservative and premised on the understanding that NewLaw is, well, New, so they almost certainly have not approached optimal quality and efficiency just yet.

But at a multiplier of $2.00 and since NewLaw is now at least a $25-billion/year business (US domestic market only), that means on the order of $50 billion taken out of what would otherwise have been the topline of law firms. To be sure, some fractional amount of the $50B probably came out of in-house spending, so it may not all have been a pure law-firm haircut.

However you slice it, if you take these trends and estimates honestly, you ought to be asking yourself if high leverage should still be one of the demi-gods in your management shrine.

But there’s more, and it comes back to clients. You are in the distinct minority if you haven’t heard this observation or its equivalent: “I’ll happily pay $1,000/hour for the partner who’s the go-to name on this kind of stuff; it’s the $350/hour associates that are killing me.”

Or: “We’re partner-service driven.”

Or: “15 minutes with [Dave] is worth all day with someone else.”

Or even (from a managing partner): “There is literally no hourly rate high enough to capture the value of [so and so superstar’s] expertise; how on earth can I charge for this guy?”

All these remarks point in the same direction, and higher leverage is not it.

Finally, for those of you who harbor a secret fear that lower leverage –> lower profitability, I have one word for you: Wachtell.

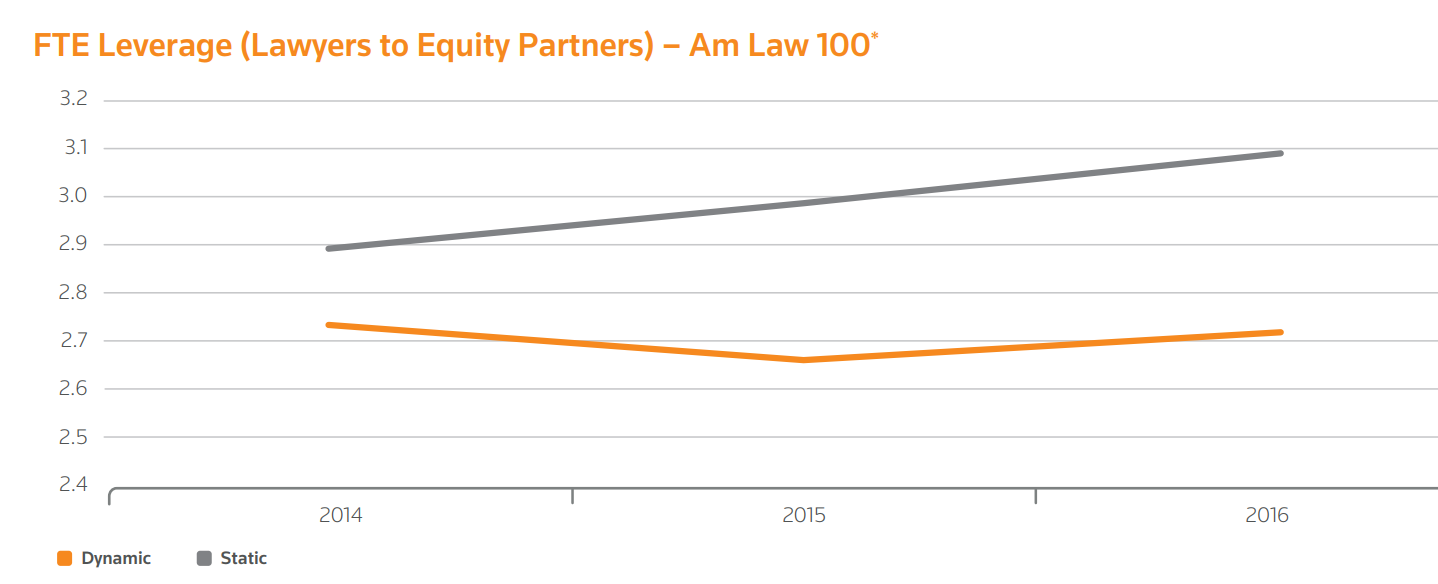

I mentioned a first whiff of data in support of this hypothesis. It arrived earlier this month in the form of Thomson Reuter’s first-ever Dynamic Law Firms Study: What Makes a Law Firm a Dynamic Industry Leader?

Here’s the executive summary of the report:

The latest study from Thomson Reuters Legal Executive Institute highlights a few areas where some firms have been able to set themselves apart, and provides some guidance as to areas where law firms looking for additional growth may want to focus.

The 2017 Dynamic Law Firms Study is based off an analysis of firms participating in Peer Monitor, and identifies those law firms that have seen best-in-class growth over a three-year period in the key areas of revenue per lawyer, overall profits and profit margin. We conducted an analysis of the entire Peer Monitor universe, calculating the compound annual growth rates for each firm on each of these metrics. Firms were then scored based on their performance on each metric, and placed into quartiles based on their composite score. The upper performing firms — those with the best composite scores reflecting strong growth in these areas — became our Dynamic Law Firm population. The lowest quartile firms — those who have experienced slower growth in these areas or in some cases even contraction — became our Static Law Firm population.

Now, then: Here’s the data on leverage among the AmLaw 100 “dynamic” (orange) and “static” (gray). Not only are the dynamic firms operating at about 10% lower leverage (2.7:1 vs. 3.1:1), they’re not growing it–and the static firms are.

Could this be a leading indicator of the death of one of the most time-honored of law firm financial tuning tools? And what would it mean if it is?

Well, just for starters it might mean firms would want to invest more in junior talent–recruitment, retention, training, enrichment–as the beginning of a return to the days when partners could welcome first-year associates with a straight face and say, “We hope each and every one of you makes partner.”

Isn’t that, after all, the way most companies in the economy work, or would like to work? To keep people as long as they can, given continuous and appropriate improvements in performance? To become a firm of loyal team-mates?

What would be wrong with that? It might even lure more highly-qualified college grads back to the doors of Upper Crust law schools.

Excellent piece Bruce, uncompromisingly hitting the mark. One question from me: You state “NewLaw is now at least a $25-billion/year business (US domestic market only)”. Based on the size of the big NewLaw enterprises of which I am aware, I find this figure hard to agree with, e.g. the reported annual turnover of Axiom Law is $300m. Of course, the definition of the industry is key. My January 2015 post is a comprehensive attempt to define NewLaw: http://www.beatoncapital.com/2015/01/fresh-thinking-evolving-biglaw-newlaw-continuum/. Welcome your comments. All the best George

I wonder if there are ties to ASE’s “A New Taxonomy: The seven law firm business models,” that are worth considering in regard to “leverage?” In consulting engineering, there are two, quite distinct manners of generating income: a) “extension of staff” and b) specialist consulting. The former is the provision of qualified and supervised, usually low- to moderate-experience staff who undertake functions that Client *could* execute via full-time, in-house staff if they saw that as the best use of resources. The latter is the provision of highly experienced specialist engineers who develop the conceptualizations for, then oversee the execution of complex programs for which there are “existential” implications for client (say, a water-retaining dam upstream of population or a sensitive ecological reserve), and “stamp” the final designs as compatible with their responsibilities to both Client and the public. Engineering consulting firms routinely leverage the extension-of-staff function, but the fees for the engineering boffins are already so high (relative to industry) that there is little elasticity and so limited capacity to provide marginal revenue.

In these conditions, an engineering firm must make a fundamental decision about the nature of its business. Although many engineering firms will assure you that they can do it soup-to-nuts, it is of no use, or even interest, to Client A that Consultant X has 87,000 employees world-wide. Readers here can easily match up Bruce’s “New Taxonomy” categories with the role of leverage in terms of how the law-firm models relate to “extension of “staff” versus boffins.