From the foregoing analyses, it is apparent that the financial performance of law firms over the past 10 years has been driven by only one factor: rate increases. As we have seen, demand gowth for law firm services has been essentially flat, productivity has been declining, expenses have been growing (albeit at a fairly modest rate), and leverage has remained essentially unchanged. In short, the only factor positively impacting revenue growth has been the ability of firms to raise rates 2 to 3 percent a year.

—Thomson Reuters Legal Executive Institute/Georgetown Law Center for the Study of the Legal Profession, 2017 Report on the State of the Legal Market (January 2017)

There are two kinds of companies, those that work to try to charge more and those that work to charge less. We will be the second.

Your margin is my opportunity.

—Jeff Bezos

Just released is the annual Georgetown/Thomson Reuters Report on the State of the Legal Market, 2017 edition. What does it tell us?

Frankly, if you’ve been paying attention to these pages for awhile, nothing new. Rather, it reconfirms, recements, and underscores trends we’ve seen developing and commented upon and analyzed for quite a few years.

That’s not 100% accurate: There is actually one surprise, in the form of recasting and putting a valuable new spin on the debate about the durability of the billable hour, but to learn what that is you’ll have to plough ahead here. (Writer’s prerogative and besides, it’s only fair.)

What’s confirmed is this:

- The Great Financial Meltdown shocked the law firm world from a sellers’ market to a buyers’ market, and clients aren’t going back.

- The primary economic and financial consequence of that is unrelenting pressure on fees.

- Second order effects include a revealed preference by clients to avoid 1st and 2nd year associates wherever possible (with law firms responding, mirabile dictu, as rational service providers and cutting their professional ranks at that level).

- Enforced disaggregation of services away from the law firm as the all-purpose supplier to a mixture of what law firms are best at and what contract, staff, and temp lawyers are best at, as well as to: Legal process outsurcers; business model optimizers; technology; and more, is the order of the new day.

- New entrants and new competitors supplying legal services, of which law firms are only a subset cohort, are here to stay. Indeed, every plausible statistic I’ve seen on this is that the “non-law firm” segment of the legal services market is growing far faster than overall demand, meaning it’s doing so pretty much entirely at the expense of traditional law firms.

- Pressure on fees expresses itself in many forms, but the more familiar ones include steady erosion of actual billed and collected rates; productivity; realization; and profitability.

Another, more disturbing, message comes through unmistakably, at least to the attentive and open-minded reader: Much of what firms have been doing for the past decade to cope with the new world order amounts to digging the moat deeper and building the castle walls higher. In other words, we’ve devoted almost all our energy to protecting and defending the entrenched “business as usual” mindset and model, instead of exploring creative and unconventional approaches to adapting and being agile.

The athletes out there will know instintively or by hard experience that stiffening one’s spine (and everything else) in the face of an imminent impact accomplishes really only one thing: Dramatically raises your probability of injury. Smart athletes who plan to keep playing become supple, relaxed, and flexible. The wisdom of this, by analogy, is that when something bad is about to happen to you, relax and absorb the blow so you can devote your energy to recovering and re-entering the competition—having learned something about how not to get in that very situation again.

Maybe not enough lawyers are natural athletes.

Jim Jones (a friend) summed it all up nicely:

“It has been a difficult 10 years for law firms in many respects, and looking ahead, significant long-term challenges remain,” said James W. Jones, a senior fellow at the Center for the Study of the Legal Profession and the report’s lead author. “Actions that have helped sustain firm financial performance over the past few years, such as expense controls and reducing the equity partner ranks, are not likely to be as effective in the future. Firms need to embrace a longer-term, fundamental shift in the way that they think about their markets, their clients, their services, and their futures.”

So much, in other words, for reinforcing those moats and walls. Gunpowder has been discovered.

I promised a novel goody for those who pressed on past this article’s introduction and here it is. The Georgetown report breaks with past custom and practice—one followed here at Adam Smith, Esq., in fact—and recategorizes pricing and revenue arrangements that have their roots in the billable hour—but include fixed-prices, caps, and/or budgets—as full blooded Alternative Fee Arrangements, and not as mere changes being rung on what is at heart a billable hour paradigm.

At a stroke this boosts the market share of AFA’s from the 15 to 20% estimate we’ve all become accustomed to, to as much as 80 to 90%. If the authors simply declared this semantic shift ex cathedra, you (and I) might quibble, but on reflection I think they have a point. Fee arrangements that may have their historic and cost-accounting roots in the billable hour world take on a very different cast in reality when caps are superimposed:

Plainly, the imposition of budget discipline on law firm matters forces firms to a very different pricing

model than the traditional approach of simply recording time and passing the associated “costs” through

to the client on a billable-hour basis. In fact, from a law firm standpoint, a budget approach is in some

respects worse than an AFA, since it imposes a fixed price (in the form of the budget cap) but forces firms

to “earn their way up” to the fixed price through recorded billable hours (which may themselves be deeply discounted). Moreover, even if the budget caps imposed by clients are subject to renegotiation on some basis, the existence of the budgets themselves may result in self-imposed restraints on partners to push for adjustments. Firms may choose to regard these budget-driven arrangements as billable-hour-based pricing, but they are substantially different from the traditional model that largely prevailed prior to 2008.

The final point is the one that brought me ’round on this. Fees set under such provisions bear no meaningful economic kinship with the Classical Era Billable Hour, which was a cost-plus pricing model par excellence.

I want to pursue the question of the primacy of the billable hour in a slightly different context, but first may we pause to celebrate its evident diminution in importance in pricing?

Let us recall what’s intrinsically wrong with the billable hour as a revenue model:

- It begins life in “cost of production,” not “value to client;” this is probably its Original Sin. Do I care what it cost to produce a BMW, a dress suit, or for that matter a restaurant meal or a haircut? Not a fig: Never have, never will. I care first and last about its value to me.

- Obviously, it rewards the law firm for being inefficient; this is such a fat pitch it’s almost embarrassing to mention it.

- Somewhat more subtly, and I believe more corrosively, it places 100% of the risk of the engagement in the client’s lap and not the firm’s. Whatever happens to the client as a consequence of their encounter with Law Land, the firm gets paid and paid handsomely.

This bill of particulars is familiar enough.

Do the Thomson Reuters findings mean the billable hour is defanged?

Alas, no. The problem is more insidious and deeply ingrained: Almost every metric firms use internally to measure and reward or penalize profitability margins, compensation, and lawyer performance is billable-hour-driven. This assumption is so deeply instilled in lawyers that many have a hard time imagining it could be otherwise. But it not only could be, it needs to be:

To remain competitive in the rapidly changing market for legal services, firms must bring all of their systems and processes (including pricing, evaluation, compensation, resource allocation, and others) into alignment around consistent principles of profitability. Continued reliance on the traditional billable hour approach for all (or even some) of these purposes no longer makes economic, competitive, or practical sense.

A final thought.

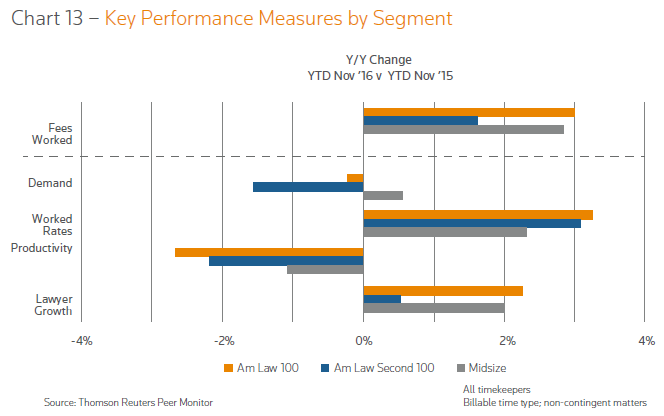

The close reader of the Report will have noted Chart 13 on page 13, which, if you ask me, contains a powerful message.

Three Firm Segments Performance

The chart displays just 11 months of 2015 vs. 11 months of 2016, but the narrative tells us what happens if you extend the comparison period to a three-year span: Every trend shown here becomes stronger and more pronounced. Those trends are simple. Here are the winners on each of the metrics shown:

- Fees worked: AmLaw 100 and Midsize

- Demand: AmLaw 100 and Midsize

- Worked Rates: AmLaw 100 and Midsize

- Productivity: AmLaw Second 100 and Midsize

- Lawyer Growth (not meaningful in terms of “winners and losers”)

The story as I read it is that you want to be an AmLaw 100 or a Midsize, but probably not an AmLaw Second 100.

That’s grossly simplistic, of course, but nevertheless or faithful authors offer an hypothesis which could explain these results, and I happen to buy it (emphasis supplied):

One possible interpretation of these results is that clients, while still directing some types of work to highend, fairly specialized, premium firms (the Am Law 50), are increasingly willing to move substantially down market to smaller firms (midsize firms) in order to achieve significant price savings. If the large firms in the middle (the Am Law Second 100 and some of the Am Law 51-100) cannot offer sufficient differentiation for their services, clients will have little incentive to change this behavior.

Yes, it’s our old friend nemesis The Hollow Middle.

The Hollow Middle dynamic is simplicity itself, and is quite widespread in the economy as a whole. Clients want the premium, high-end version of Purchase X [car, clothing, food, personal grooming] or they want to save money and economize on whatever is good enough, but the undifferentiated, not-great-not-cheap, offering languishes.

I don’t want to press an analogy past what it will bear—I studiously endeavor to leave that to others—but today’s New York Times featured an analysis of the accelerating decline of Sears, a totemic American retail brand if ever there were one, but now projected to lose more than $2 billion this year alone and “in the retailing dead pool.” The headline was Sears sells something for everyone; That’s its problem.

Amazon is not its problem: Last time I checked, Amazon had “something for everyone,” and it doesn’t seem to be hurting Amazon. No, here is Sears’ problem:

Despite the conventional wisdom, though, it is not Amazon that is primarily to blame for Sears’s plight. Sears is being squeezed by changing economies and technology. Shoppers go to Walmart for discount items or to Target for discount items with a touch of style. The high end stays at stores like Nordstrom. The middle is smaller and increasingly shops online.

(You knew I’d work Amazon in here eventually.)

Perpetually raising prices to grow revenue is like perpetually cutting costs to grow profits. You can’t play that game forever.

We seem to have pretty much concluded that we’ve played out our hand in terms of cutting costs. Private equity guys would have a different view, but firms run by lawyers are from another financial-management planet. We’ve laid off all the staff we have a heart to and we’ve de-equitized everyone we can without too blatantly shattering the Brass Ring compact. So, as the Report conclusively demonstrates, we’ve spent the last mediocre decade raising rates every year. That is beginning to provide everyone in the legal services industry who’s not a law firm—there are lots of them, and more all the time—their opportunity, as Bezos instructed us at the top.

If our new non-law-firm competitors seize their chance, it will be because we’ve rolled out the red carpet.

Each of us better figure out how we can turn our firm into Walmart, or into Nordstrom, because selling something for everyone means offering nothing compelling to anyone.

While I agree that law firms can learn quite a bit from the restructuring of the retail industry, so many of Sears’ wounds are self-inflicted that have very little to do with the market position it occupies . But Macy’s and The Gap are suffering similar setbacks, so point taken.

The dominant method for retailers to move out of the middle and to the “low cost provider” side of the spectrum is essentially an economies of scale play, primarily through pricing power/control over suppliers and keeping labor costs down. Except in the limited form of labor market arbitrage, no analogous methods currently exist for law firms serving the vast majority of SophisticatedLaw clients. Even if the motivation is there, not sure this is really an option for most AmLaw 50-200 firms as currently composed without a ruthless restructuring of most partnerships.

Skeptic: First, thanks as always for your thoughts.

Perhaps I shouldn’t have picked on Sears per se since they have been on a (largely self-inflicted, I agree) downward slide for a couple of decades, perhaps starting with the arrival of “category killers” like Home Depot and Lowe’s, to which they had no effective answer. And we can all draw distinctions where we choose–it’s something lawyers excel at!

I also agree that opportunities for labor market arbitrage in Law Land (the armies of staff and temp lawyers standing at the ready) are limited and essentially a holding action. Seriously cutting costs requires a clean-sheet-of-paper rethink of the business process model.

But perhaps, as you conclude (and as you’ll see in my forthcoming book, Tomorrowland), the greatest obstacle to fundamental change is our very own partnership model.