The first thing you learn in your antitrust law course is to ask, “What’s the market?”

In other words, define the market you’re talking about, because the definition you select, I promise you, will make all the difference. Antitrust analysis aside, choosing the span of the market on which you plan to compete is such a critical part of organizational strategy that coming up with the wrong answer can be a life or death decision. Consider just one legendary misapprehension of one’s market: Western Union passed on Alexander Graham Bell’s offer to sell them his US patent rights to the telephone because…they thought they were in the telegraph business, not the communications business. And “the telegraph is all our customers need.” Well, I suppose if you put it that way, then QED.

Believe me, I don’t mean to imply that defining a market is child’s play—or that we’re so remarkably superior to and more enlightened than the unfortunate naifs at Western Union over a century ago. Consider (this is just a thought experiment) what market HBO is in. The market for original movies and TV series? The premium/subscription cable market? The TV market? The entertainment market?

Or, here’s a thornier one currently playing out before our eyes: What market are Comcast and Time Warner Cable in, for purposes of their proposed merger? Cable TV? (If so, they share access to not a single subscriber.) Broadband? “Bundled” cable, broadband, and phone? The market of “intermediaries” between consumers and content providers? Not obvious.

But enough of the dilemma.

Today I write because I fear far too many of us are making a mistake in blithely assuming we know what the “market” is for newly minted law school graduates. It’s not one market. Thoughtful observers of this precinct of Law Land have long known this, of course, but for those of you who may not have given it much thought, or for the cognoscenti who might be interested in a little data-driven dimensionalization of this reality, read on.

At the recent annual NALP conference in Seattle, Jim Leipold, the executive director, summarized the post-Great-Reset market this way:

- fewer entry-level private practice jobs

- lower average starting salaries

- higher unemployment and under-employment

- fewer JD’s working as lawyers

- (and as a corollary) more working in business, “law-related” fields, or seeking entirely different careers

- new grads competing with displaced lawyers

- and overall a job market that is “tough across all sectors.”

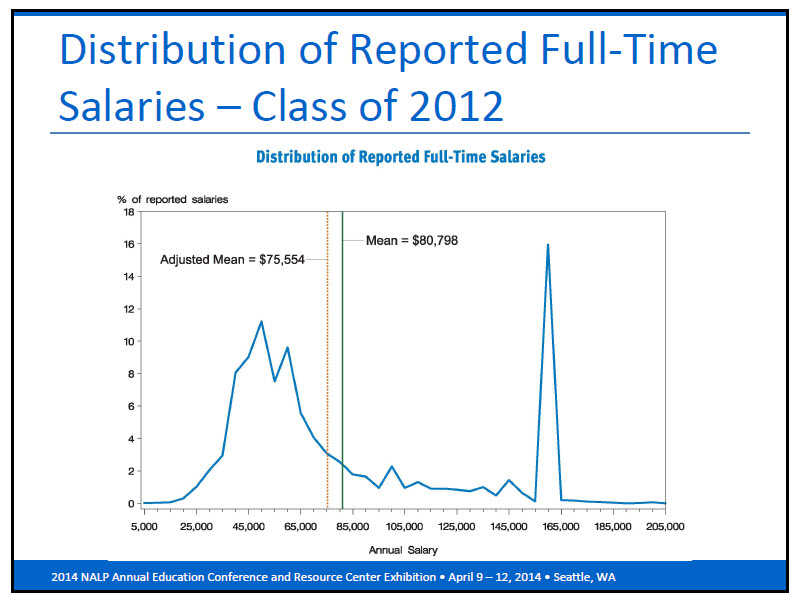

That’s from the 30,000 feet perspective. But Jim also updated what he called “my favorite slide of all time,” the bimodal salary distribution of new graduates. (NALP also gets credit for discovering this bizarre distribution when it first emerged, starting ca. 2000, and they’ve faithfully updated it ever since.)

By the way, you can click on any chart in this column to see it larger, in a new window.

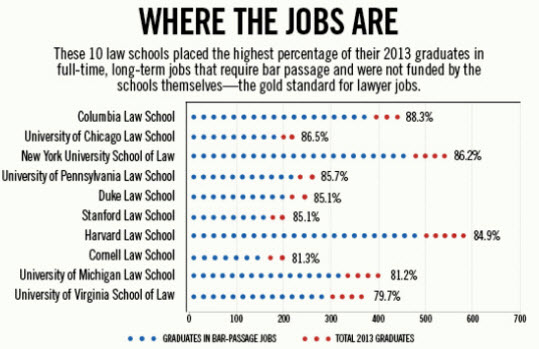

A few days ago the National Law Journal published “Bright Spots Amid Glum Jobs Outlook,” which opened, “It’s a tale of two law schools—or, more broadly, of two legal education worlds.” It doesn’t get much more direct than that. What has to be surprising—certainly to any outside observer and I imagine to anyone who hasn’t dwelt a bit on the data lately—is how great the chasm is, and how precipitous is the drop from the best-performing law schools in terms of placing their graduates in the gold standard of lawyer jobs, namely those that are:

- full-time

- long-term

- requiring bar passage

- and not funded by the schools themselves.

Here’s the opening chart listing the top 10 schools on that metric: Columbia, Chicago, NYU, Penn, Duke, Stanford, Harvard, Cornell, Michigan, and UVa (schools are ranked top to bottom by total percentage scores, from Columbia at 88.3% to UVa at 79.7%; the horizontal axis is the total number of 2013 graduates, showing Stanford [for example] as a relatively small school and Harvard as large).

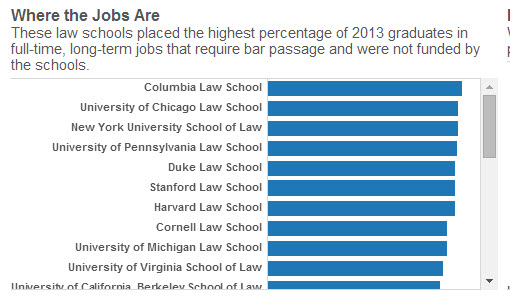

Note that as soon as you descend below the top ten schools you are already into fewer-than-four-out-of-five graduates getting these gold standard jobs—and there are more than 190 schools to go. You can view the same data this way if you’d like:

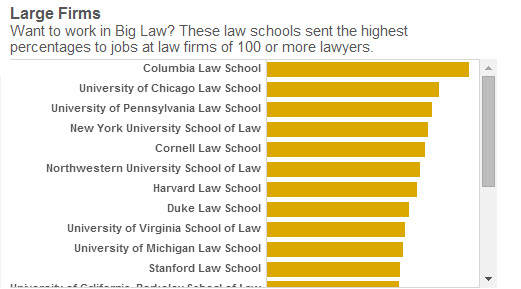

or chart it down by percentage of grads in “BigLaw” jobs (firms > 100 lawyers):

and at the opposite end of the spectrum you can look at unemployed (here the statistics top out at nearly 50%)

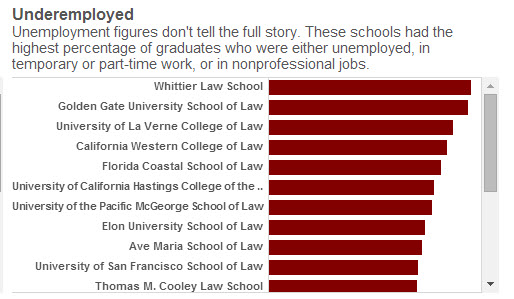

and underemployed (defined as unemployed plus those in temp or part-time work, or nonprofessional jobs) (topping out at nearly 60%)

Not to pick scabs, but just as we see the usual suspects among law schools at the top of the heap, we see the same crowd at the bottom—of the eleven schools identified on each of these last two charts, nine schools are on both.

One last chart, and a concluding thought. This is from the estimable and praiseworthy “Law School Transparency” project, and it shows the top schools by graduate employment rates as well—confirming our now presumably settled expectations of who’s at the top of the pecking order.

This runs from #1 UVaat 95.6% to #22 Iowa at 76.3% (different methodology from the NLJ’s, supra)

You may be tempted about now to wring your hands and turn on HBO. But I actually have some thoughts about how to help alleviate this depressing situation, in the form of a new initiative that has hit the ground running. I’ll report on that in the next few days.