Legion are the topics lawyers don’t talk about, and they could perhaps be accurately summarized as “anything we’d prefer not to talk about,” but primary among them is the strength or weakness of their own firms’ business models.

So that’s our topic du jour.

A couple of weeks ago Bill Gurley, who’s a VC with Benchmark Capital and an all-around smart guy (I don’t know him personally), published one of the best articles I’ve seen recently on what characteristics contribute to a strong business model. He called it All revenue is not created equal: the keys to the 10X revenue club and it’s one of the most insightful shortish pieces I’ve read about what companies that deserve high valuations have in common.

I mentioned it in a recent piece here on Adam Smith, Esq., but now I want to discuss how it does, or doesn’t, apply to the classic law firm model.

First of all, Bill talks about the ubiquitous financial tool of discounted cash flow (DCF), which he describes as follows:

What drives true equity value? Those of us with a fondness for finance will argue until we are blue in the face that discounted cash flows (DCF) are the true drivers of value for any financial asset, companies included. The problem is that it is nearly impossible to predict with any accuracy what the long-term cash flows are for a given company; especially a company that is young or that might be using an innovative and new business model.

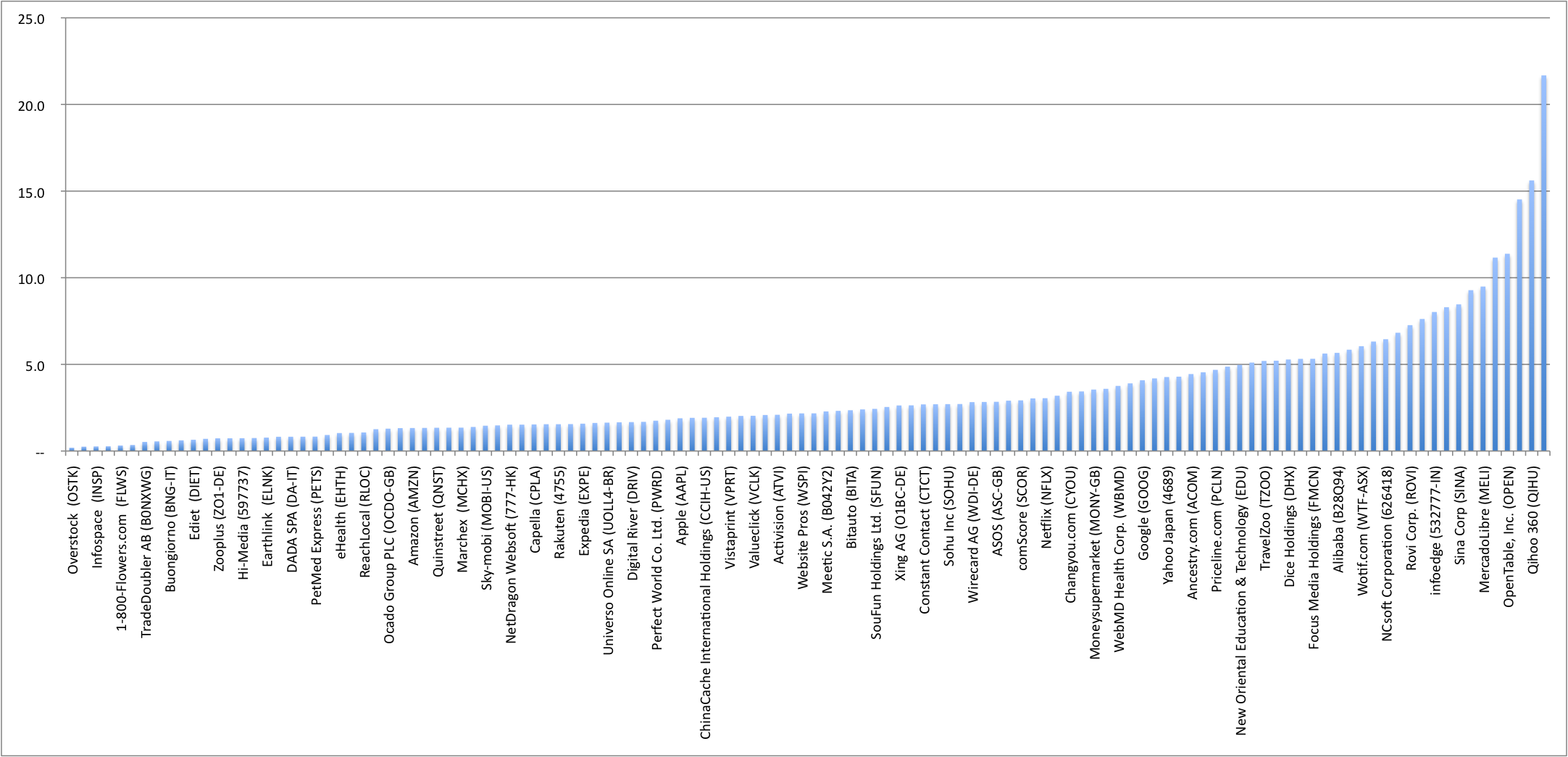

So people turn to other metrics including such problematic measures as price/revenue or price/sales ratios. The difficulty with these is how widely dispersed they are: Just take a look at this graphic.

For those of you who can’t read the fine print, this distribution is of 122 global Internet stocks for 2012 forward price/revenue ratios, and goes from Overstock at the extreme left at 0.2x analysts’ 2012 revenue estimates to Youku.com at the other end, the leading Chinese video website, at 21.7x analysts’ average 2012 revenue estimates. (LinkedIn went public after this chart was compiled.)

The first and most important observation about this chart is that there’s a long tail to the left: That is to say, most companies have a relatively low price/revenue ratio; only the exceptions score very high. In fact, Bill does the math and reports that 72% have a multiple below 4x and only 5 (4%) are above 10x.

Of course startups can also turn to all sorts of other creative accounting measures, as recently humorously summarized in this NY Times piece, “Abracadabra! Magic Trumps Math at Web Startups.”

Since I happen to have a startup of my own at the moment, I read this with more than academic interest, and decided that henceforth our financial projections would be based on what Lynn E. Turner, a former chief accountant for the Securities and Exchange Commission, once called E.B.B.S., or “earnings before bad stuff.”

But back to the 10X Revenue Club.

We’re going to now rank law firms (in general) on Gurley’s 10 scores of the 10X Revenue Club, on (inevitably) a scale of 1-10, 1 meaning not applicable at all and 10 meaning totally qualified on that count.

#1: Sustainable Competitive Advantage

What this means is fairly simple:

By far, the most critical characteristic that separates high multiple companies from low multiple companies is competitive advantage. This concept, well explained in Porter’s book by the same name, basically asks the question, “How easy is it for someone else to provide the same product or service that you provide?” If your company has “high barriers to entry,” Wall Street will be super excited, as investors will have confidence discounting cash flows many, many years into the future.

Presciently, Gurley talks about Coke vs. RIM, before the recent RIM stock price meltdown:

Coca-Cola has a 5% estimated 2012 growth rate, and a 3.6x price/revenue multiple. RIM has a 12% estimated 2012 growth rate and a 0.77x price/revenue multiple. What gives? Investors expect Coke to be around in pretty much its same form 50 years from now. It is much harder to say that with confidence about RIM.

(If you haven’t already shorted RIM, it may be too late, but if you’re a bankruptcy specialist, you might want to start getting to know their Board of Directors).

Law firms’ score on this, from a scale of 1-10: 1. Why so low? Primarily because our key supply, lawyers, are so mobile. If a firm starts to falter, its lawyers will prove far nimbler than they ever seemed to be before. Within months your firm could be reeling.

# 2.The Presence of Network Effects

No discussion of competitive advantages and barriers to entry is complete without a nod to perhaps the strongest economic moat of all, network effects. In a system where the value to the incremental customer is a direct function of the customers already in the system, you have a powerful dynamic that tips towards winner take all.

Perhaps the most important thing to say about network effects is they’re claimed to exist far more frequently than they do exist.

Law firms’ score: 1.

Think I’m grading too hard? The criterion here, remember is network effects, not whether having IBM as a client makes you more attractive to GE and Exxon. The latter is not a network effect, it’s a reputation effect (see below).

#3: Visibility/Predictability Are Highly Valued

For the same reason that investors favor companies with sustainable competitive advantages, investors favor pricing models that provide a high level of predictability and consistency in the future.

…The more certain you can be of future cash flows, the higher premium you will put on a business, and as a result, you will see a higher price/revenue multiple. One obvious example of this is the predictable nature of SAAS subscription revenue. Salesforce.com trades at a staggering 7.5x 2012 estimated revenues.

Consider the classic law firm model. Do we have “subscribers” as clients? Is their return predictable and consistent? Redwood Analytics famously did a study a few years ago showing that the average decay rate of clients across a sample of AmLaw 100 firms was 1%/month. 1%/month means you lose one-quarter of your clients in 2 years.

Law firms’ score: 3.

Yes, loyal clients are loyal, but a change of GC at the top, the retirement or defection of a key partner, and the reliable client quickly becomes the fond memory.

#4: Customer Lock-in / High Switching Costs

If investors value predictability, then retaining customers for long periods of time is obviously a positive. Conversely, if customers are churning away from your company, this is a huge negative.

…For non-subscription businesses, customer-switching costs also play an important role. If it is relatively easy for your customer to switch back and forth from your products to you competitors, you will likely have a lower price/revenue multiple as your pricing power will be quite limited. On the other hand, if it is quite difficult for a customer to switch away from your product/service, you are likely to have stronger pricing power, and longer customer life,

Law firms’ score: 3. It might be more accurate to segregate firms into those who score a 1 and those who score a 6. Some firms do have institutionalized clients, and some have none. 1 for the latter, 6 for the former. Tie-break: 3.

#5: Gross Margin

Pretty basic. And, for a change, law firms generally have very attractive gross margins on paper—in the range of 30-45% and up, based on my own experience backed up by American Lawyer reported results.

Or do they?

Those reported margins are before paying partners. This makes a shocking diference, especially because most firms strip-mine their balance sheets of cash at the end of every fiscal year in order to pay out partner distributions.

Economically, the correct analysis of what a firm’s real gross margins are would subtract out what all partners’ “going rates” for competitive compensation on the open market would be before arriving at a profit figure. After all, it’s more than a bit perverse to pretend that your gross profit margin can be calculated without paying a cent to the senior cohort of people producing the services you sell.

Law firms’ score: I’ll give us a 3.

#6: Marginal Profitability Calculation

“Marginal [incremental] profitability” is a measure of whether a company’s business model scales. You calculate it by comparing incremental revenue and costs in period 2 vs. period 1. If revenue grew faster than costs, there are economies of scale and incremental operating margin will be positive.

Investors love companies with scale. What this means is that investors love companies where, all things being equal, higher revenues create higher profit margins. Microsoft had wonderful scale in this manner for many, many years.

…In order to measure how a business is scaling, many investors look at marginal incremental profitability. … Simply look at the change in revenue versus the change in costs, and then calculate the incremental operating margin of the two results. If this marginal profitability number is much higher than historical profitability, a company is scaling nicely.

….This is also the reason that “human capital” businesses like consulting businesses often have trouble with low valuations on Wall Street. If the majority of costs are people, and people are also the key input for any work product, you will find the ability to generate increased marginal profitability quite difficult.

Nicely put, that, isn’t it? “[If] people are the key input, you will find the abilitly to generate increased marginal profitability quite difficult.”

Law firms’ score: 1.

#7: Customer Concentration

In their S-1, companies are required to highlight all customers that represent over 10% of their overall revenue [which is for a reason because it’s a risk factor]. […] The ideal situation is tons of very small customers who are essentially “price takers” in the market.

Not a problem for most firms. Indeed, the reverse is the problem–an incredibly perverse long tail or little tiny baby clients.

Law firms’ score: 10.

#8: Major Partner Dependencies

Investors will discount the price/revenue valuation of any company that is heavily dependent on another partner is some way or form. A high profile example of this is Demand Media’s reliance on Google’s SEO traffic.

Not remotely germane for most law firms.

Law firms’ score: 10.

#9. Organic Demand vs. Heavy Marketing Spend

All things being equal, a heavy reliance on marketing spend will hurt your valuation multiple. […] You will be hard pressed to find a company with a heavy marketing spend with a high price/revenue multiple.

Law firms don’t really have “heavy marketing spend,” but they can have a greater or lesser reliance on partners’ taking time from billable activity for active business development. The real key here is whether you do or don’t have “organic growth.”

Unless you’re truly exceptional, you don’t have “organic demand.”

Most of the companies that have really high multiples, and that have been highly respected by investors all have or have had organic growth: Yahoo, Ebay, Google, Facebook, Skype, OpenTable, Baidu. These business models did not require marketing.

Understand what Gurley is saying: It’s not that these firms grew without marketing; it’s that their customers did it for them. Gurley points out that the marginal cost of adding a new user to Skype was $.001 whereas for Vonage it was $400. Which model is your firm closer to?

Law firms’ score: 3. Word of mouth is something but your clients’ doing your marketing for you is still for most firms a dream devoutly to be wished.

#10: Growth

We saved the best for last. Nothing contributes to a higher valuation multiple like good ole’ growth.

Swell, I hear you saying, and you’re right. Growth has gone from “coming with the territory” to, for all but the luckiest firms, an ugly fight for market share.

I don’t know where on that spectrum your firm stands, but from ca. 1980 to September 15, 2008 (the fall of Lehman), virtually every AmLaw 200 firm said their strategy was Growth, or at least behaved that way.

No more.

So now what?

Law firms’ score: 3.

Where does this leave us?

Numerically, it leaves us at a score of 37 out of a possible 100.

But there are of course two outliers on this scoring: (1) We tend not to depend for a lot of our revenue on one or two key clients and (2) We don’t have major dependent relationships on key partners. Take those two scores out of the mix and we score 17 out of a possible 80.

Is it fair to take those two measures out?

Reasons it’s unfair: Gurley included them in his scorecard so the scorecard is the scorecard.

Reasons it’s fair: They actually aren’t diffferentiators in any meaningful fashion in our industry. It’s not as if some law firms have those characteristics and some don’t; no law firms have those characteristics. So in comparing law firms to law firms, they’re beside the point.

Debate those points among yourselves.

But for my money: Do we have a strong business model?

Inherently not.

We’ll bypass for today what this might mean in terms of our attractiveness to private equity and their comrades in arms come the effectiveness of the Legal Services Act in the UK later this year. Let’s just focus on what we can do about it.

As I see it, the implications are pretty straightforward:

- Leadership matters

- Strategy matters

- Differentiation matters

More than they ever have as long as I’ve been a student of this industry.