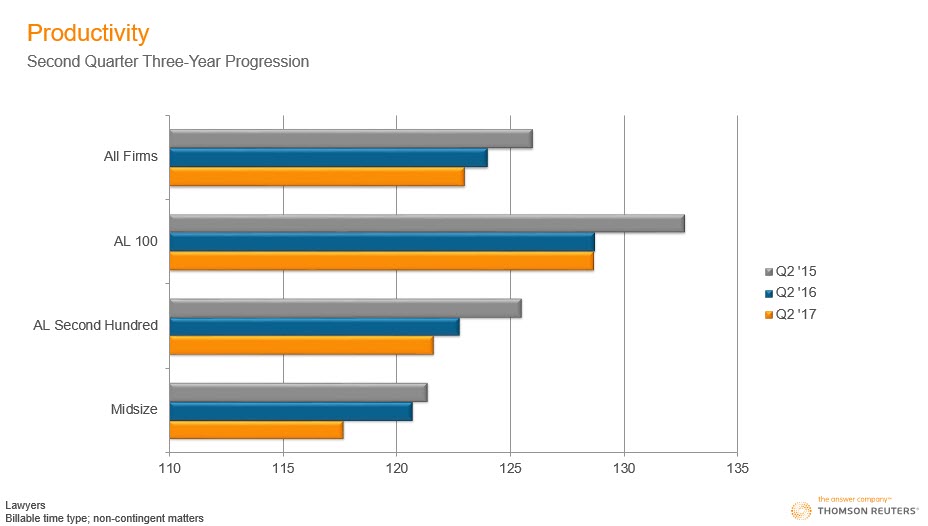

It has not looked healthy for firms in any segment over the past three years: Here’s the data on billable (non-contingent matter) time for the 2nd quarter of the most recent three years, in hours per lawyer per month:

Let me spare you the math: Extrapolating the Q2 results to a full year produces annual hours of 1,400 for the least busy cohort (“midsize”) and a hardly lofty 1,525+ for the hardest working (AL 100). Either would have meant the door for an associate, and raised eyebrows for a partner, as recently as, say, when today’s first-years were starting high school.

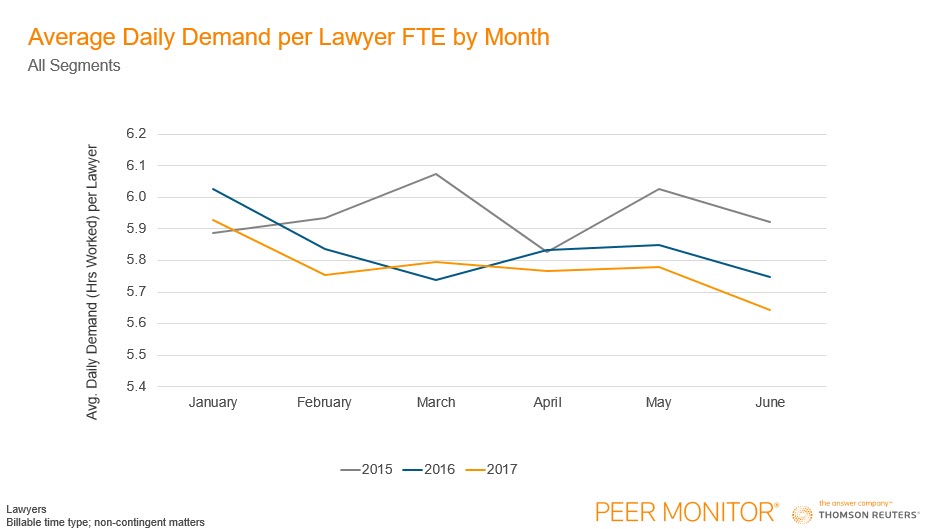

A final, ugly, portrayal of the data. Here we have average daily demand for the first six months of the past three years. The most telling observation about this is that at no time was the 2017 trend line the highest line on the chart.

These numbers on “productivity”/utilization are firmwide figures not broken down by practice area, so it would be fair of you to ask how is this germane to litigation exactly?

Believe me, if I had the data segmented into transactional and litigation, I’d show it to you but I don’t so I can’t. I’m unaware of any reliable industrywide sample dataset that can be filtered that way (but if you know of one, pipe up!). Bear with me while I float an hypothesis about what these figures mean.

We know that for nearly a decade, demand for transactional has actually been growing (not great, but >0), but litigation has been flat. We also know that total lawyer headcount in the firms in the Peer Monitor universe has been growing. Finally we just presented various windows into how people on average are less busy. My hypothesis is that it’s likely that more of the growing overcapacity is in the ranks of litigators than transactional types.

Finally, consider:

- Law firms can’t and don’t and never will engage in anything remotely resembling “just in time supply,” at least in the core firm itself (setting aside contract and third-party supplied lawyers, which aren’t reflected in the Peer Monitor data anyway).

- There is thus a lag, usually a looong lag, between secular changes in demand for a practice and the firms’ headcount devoted to that practice. There’s also denial and temporizing about whether the decline in demand is, in fact, secular. Some of this is rational.

- When an industry or a market sector is afflicted by excess capacity and enters the land of a battle for market share, there is a non-rational but almost irresistible temptation to shave prices to maintain share and keep people busy. Even if “busy” has to be continually defined down.

- We began this series by noting that across BigLaw, litigation has historically accounted for something on the order of 30-45% of revenue, and when the billable hour is your revenue model, that translates linearly into 30-45% of your lawyer headcount. That’s a large chunk of the firm to “right-size” quickly.

- QED: We have a lot of less-than-100% busy litigators.

In our next installment we’ll discuss how (a) the ever-increasing power of e-discovery tools, especially as applied to early case assessment, and (b) the predictive power of AI, will affect litigation as a law firm practice area.

Battle for share, anyone?