He observes that given this revenue-constrained environment, the best—in some cases the only—way to grow profits has been to cut costs. As he puts it, “synergy” is now back, only it’s called “savings.”

There’s another way to look at mergers acquisitions: Those that are driven by “financial” buyers vs. those that are driven by “strategic” buyers.

As you might surmise, analysts (and markets) rightly take a dim view of financial-engineering driven buyers. They’re generally in it to cut costs, consolidate operations, eliminate overlaps and duplicative activities, real estate, and people, and try to generate economies of scale. (We’ve often pointed out that there are no “economies of scale” in the classic, hard-core microeconomic sense, in Law Land, although we would be the first to observe that there can be real advantages to scale.) Once the costs and redundancies are wrung out, what’s next? You can’t cut your way to ever-increasing profitability, as they say.

Financial buyers tend to be of two kinds: First are the pure investors, who are (not to be oblique about it) pools of money looking for places to deploy it—hedge funds, private equity, turnaround shops—and they can require the existing and/or new management of the target to dance to exceedingly tight and unforgiving metrics. R&D and capital investment are usually the first to go, and then it’s advertising, talent recruitment, employee perks and benefits, pensions and 401k matches, and so it goes.

The second type of financial buyers are operating companies in the same sector/vertical as the target with cash on their hands or a rich stock price. The point is that operating companies who go looking for acquisitions without a driving strategic purpose are usually looking for the “inorganic” growth Citigroup cited in the Dealbook column. 2 + 2 = 4, assuming you can keep the combined firms intact after the deal.

Strategic buyers are cut of different cloth. They don’t start with cash burning a hole in their pocket (although they may be cash-rich); they start by asking what gaps in their capabilities an acquisition could address. Not “what’s in it for our balance sheet?” but “what’s in it for our customers?”

Accordingly, they tend:

- to understand the acquired business more thoroughly;

- to have a much longer-term perspective on the combination;

- to be willing to invest and reinvest after the initial purchase/combination; and

- to devote top-notch talent to making the integration take hold and work.

Now, three guesses as to which type of buyer tends to have greater long-run success.

Bringing us back to Law Land.

If you’re thinking of merging with another firm because lately (a) revenue growth has been anemic, and/or (b) your only tool for driving profits seems to be cutting costs, or (c)—bonus points for this one—it makes the partners think management is busy and doing stuff!, then be prepared for 2 + 2 < 4. (Witness the ranks of McKenna partners decamping from Dentons practically before the ink is dry.)

But if you’re focused on what key capabilities your clients need from your firm that you can’t provide, or can’t provide at the level you’d like, and you see a potential partner that would supply those capabilities like a key in a lock, then and only then can you claim to be strategically motivated.

Of course, keeping the Good Firm Ship afloat for another few years is a worthy cause in itself.

Just don’t confuse it with having a plan.

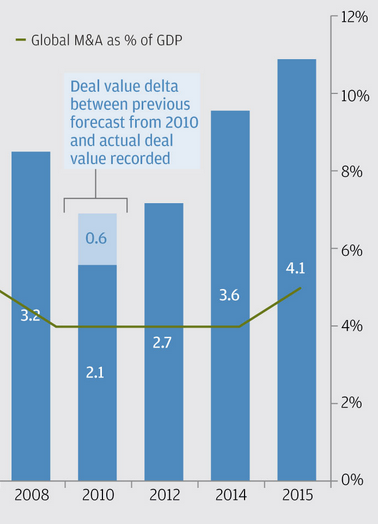

Global M&A annual deal value in $trillions (blue bars) with % of GDP on right axis (2008-2015): Courtesy JP Morgan

Bruce,

Understandably, your focus is on the firm that is considering the acquisition, their motivations and considerations. It would be interesting to have some exploration of the view-points that might be important for the firm that is being acquired.

Mark

Mark:

Aaaah, yes, the “other side” of the market! (Markets always have two sides, at a minimum.) Let me mention the two extreme ends of the spectrum, from the perspective of the acquiree, as it were: